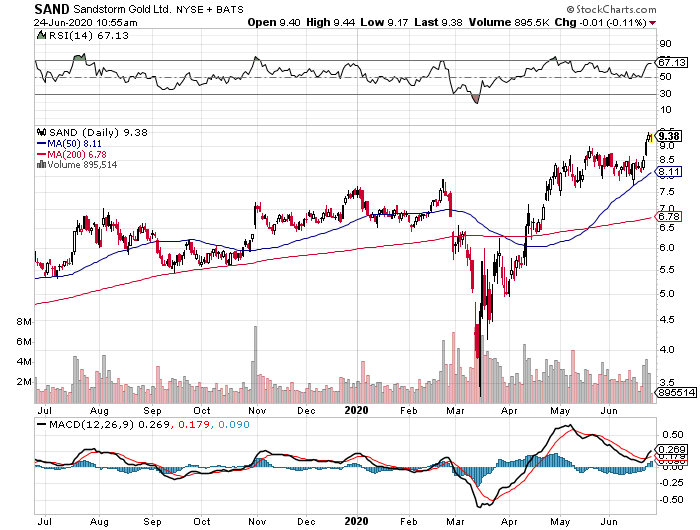

Nice breakout in SAND

Slow and steady, slow and steady

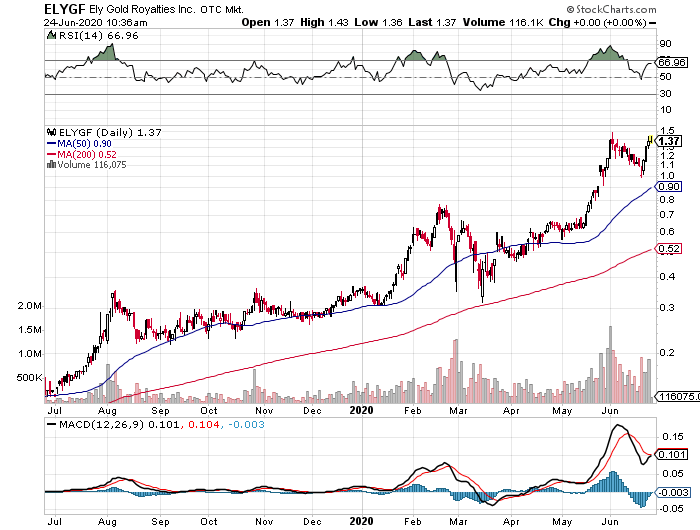

Had you bought ELYGF any time between Nov 1 and mid-January you’d be up 300%

And I’ll bet there’s another 300% coming.

Slow and steady, slow and steady

Had you bought ELYGF any time between Nov 1 and mid-January you’d be up 300%

And I’ll bet there’s another 300% coming.

I find the difference in rise between the royalty companies interesting. I have to admit I haven’t looked into it, but any idea why metalla and ely have outpaced sandstorm?

They have a different business model than SAND – both are more than royalty companies, they are a blend of royalty/project generators/investing in new mines. They each have their niche so it pays to read about their respective business models to understand what they are up to. MTA is overdue for a breakout, BTW. SAND is destined to be another WPM…but it takes time. Another really good one is EMX.

Also, the smaller (i.e. lower priced) juniors tend to deliver bigger percentage moves; nature of the beast. You’d never see SAND jump 10% in a day, for example. At least I don’t think you would at this stage.

Here’s the list of developing mines in which Metalla has invested. No royalties or streams on these yet, is my understanding:

Endeavor Silver Stream

Santa Gertrudis Royalty

Garrison Royalty

El Realito Royalty

Fifteen Mile Stream

NuevaUnión

Wasamac Royalty

Hoyle Pond Extension Royalty

West Timmins Extension Royalty

Beaufor Mine Royalty

San Luis Royalty

Zaruma Royalty

And here’s the deal on ELYGF – they have a different investment strategy that builds wealth for shareholders with some great dynamics. Smart guys!

Ely Gold Royalties is a Nevada-focused royalty investment company. We generate revenue by selling mineral properties to mining companies while retaining a long-term royalty that pays us for the life of the mine. Our business model includes the purchase of existing royalties from third parties as well as optioned sales of properties that provide ongoing revenue and eventual royalties.

What sets us apart is our unique ability to assemble valuable land packages near producing mines, which we sell with a life-of-mine royalty to mine operators.

And it would not surprise me to see EMX bypass SAND one day…

EMX Royalty Corporation has a long-standing track record of success in exploration discovery, royalty generation, royalty acquisition, and strategic investments. Our diversified, three pronged business approach provides exposure to multiple upside opportunities, while minimizing the impact on EMX’s treasury.

EMX’s business model is designed to efficiently manage the risks inherent to the minerals exploration and mining industry. Key elements and resulting advantages of our unique approach are:

We organically generate royalties through low cost property acquisition and early-stage exploration to build value, and then develop partnerships with quality companies to advance the projects, with EMX retaining a royalty interest and receiving pre-production payments.

Our organic royalty growth is supplemented by purchases of royalties from other parties, as well as strategic investments.

Cash flow from royalties, advance royalties, and other property payments are supplemented by returns from strategic investments, and provide “self-funding” operating capital for our ongoing business initiatives.

Using this model, we sustainably grow the royalty portfolio, with minimal dilution to our shareholders.

EMX’s royalty and property portfolio spans five continents, and consists of a balanced mix of precious metal, base metal, and other assets.

Thanks for the info. I’ve been a long-term holder of RGLD and just haven’t paid much attention to these others. RGLD is now paying over $1 per share dividend. Had you bought back in 2000, your dividends for a couple years would cover your initial cost plus you would have made over 60X on your investment.