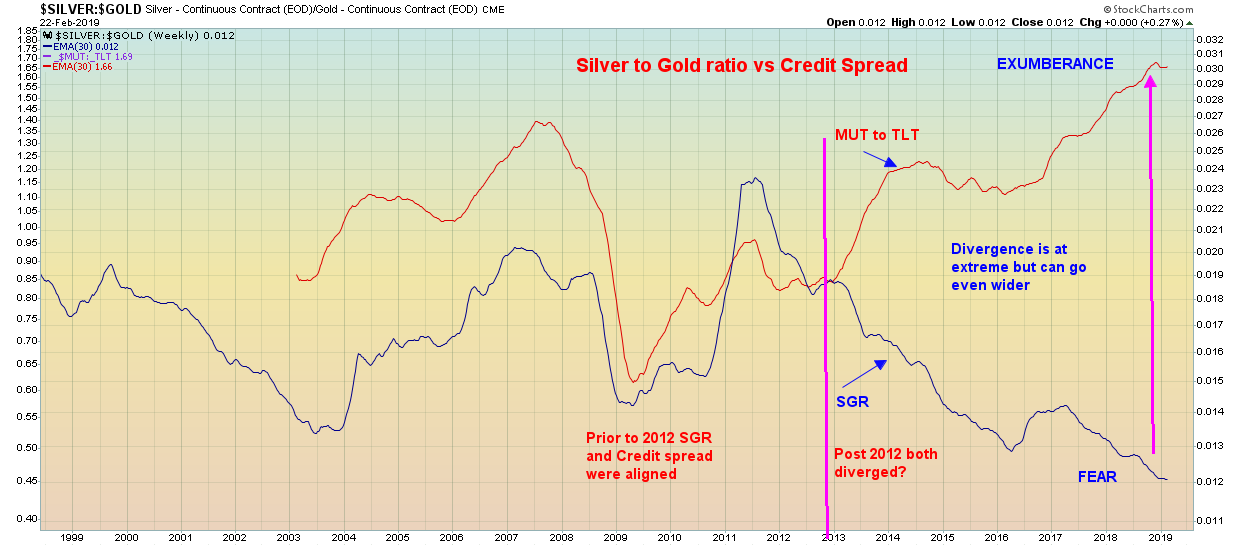

Silver to gold ratio vs Credit spread MUT/TLT

Since 2012 relationship between SGR and credit spread junk bond to treasury ratio MUT/TLT has reversed.

Going forward with credit market under scrutiny will the disparity normalize??

Signs are beginning to appear.

From one of the post:

Quote from the article “When it comes to Bubbles, the more conspicuous the less likely they are to be deeply systemic. The “tech” Bubble was obvious, yet the most egregious excess was contained within the technology sector. The mortgage finance Bubble was much more systemic, with excesses spread about and not as apparent. I believe today’s Super “Tech” Bubble is much more systemic than back in 2000. And while subprime is not the critical issue it was for the previous Bubble, I would argue that excess in many key housing markets is comparable. Commercial real estate on a national basis is likely more vulnerable today than in 2007, and the same could be said for some regional housing markets (i.e. greater “Silicon Valley”, Los Angeles, Seattle, Portland, Atlanta, etc.). Today’s Bubble in leveraged lending and M&A is greater than 2006/2007. The Bubble in corporate Credit dwarfs that from the mortgage finance Bubble period. Excesses throughout the securities markets phenomenally exceed those from the prior Bubble period. Moreover, I suspect the current level of derivatives-related speculative leverage could be multiples of 2007.”

Nice, Bikoo99 – that’s quite a connection you’ve drawn. Obviously, something is going haywire, something dark is just over the horizon. Or perhaps it will be the dawn of a new day that will be better. I suspect we will find out soon enough.