Yield Curve Flattening- John Mouldin

Implications of yield curve best explained by John Mouldin. Bob Hoye had the same prediction back in 2007 when yield curve turn from inversion to steepning.

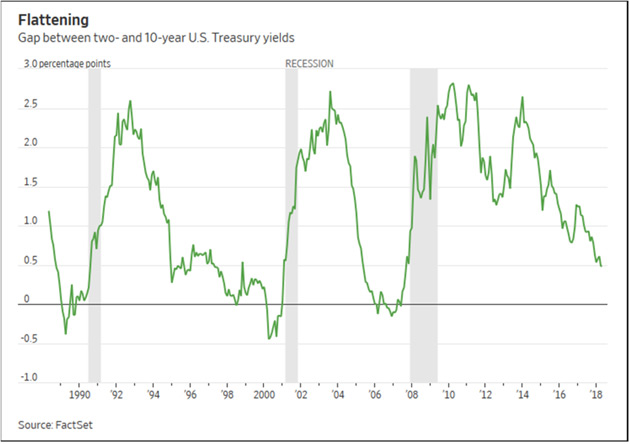

“Flattening Curve

Last week brought a little (at least short-term) good news if you’re worried about the yield curve inverting, i.e. short-term rates rising above long-term rates. The ten-year US Treasury yield rose above 3% for the first time in four years. This will be the opposite of inversion, if it persists. It makes the curve steeper unless short-term rates rise even more.

Nonetheless, the yield curve is still abnormally flat. The gap between two-year and ten-year Treasury yields hasn’t been this low since before the last recession.

Note in the graph how this gap dropped below zero—i.e. inverted—shortly before the last three recessions. We haven’t seen it yet in this cycle. But we certainly could see inversion within the next year or so if it keeps dropping at the current rate. That’s quite possible if the Fed keeps hiking because they have hit their inflation and employment targets.

The Fed is now walking a very tight rope. They know, deep down and viscerally, that they have to get rates back up so that they will have a few “bullets” for the next recession. It is likely they will keep hiking rates until we get to an inverted yield curve. Are they aware of all the literature and what they’re doing? Absolutely. Candidly, I can’t imagine accepting a Fed appointment knowing that we are this late in the cycle.

Does an inverted yield curve guarantee a recession? No, but inversions are strong evidence one is forming. Last month, yet another new San Francisco Fed study found an inverted yield curve, which predicted all nine US recessions since 1955, is still valid even in today’s low-rate environment.

However, yield curve inversion is a far-leading indicator, which is why my previous recession and bear market calls were early. Those nine recessions all began 6–24 months after the yield curve inverted. And, in the ones I’m old enough to remember, many experts spent those months telling us that this time was different. (Spoiler: It wasn’t.) And I expect the same again.

Look around at all the great economic news. I’m aware of it. But the economy was hitting on all cylinders in early 2000 and late 2006, too. The numbers always look great right before a recession. Then it all rolls over at once.

Like that fever I mentioned, an inverted yield curve doesn’t immediately damage the economy. It points to damage that’s already happening—an underlying infection. It means bond investors have lost short-term confidence in the economy and want to lock in longer-term interest rates. You don’t want to buy, say, one-year bills if you think rates will be lower when it’s time to reinvest them. That will be the case if, for instance, you expect the Fed to be lowering rates to stave off recession.

One point about that economic fever. I said that fevers don’t kill you, they are a symptom of something being wrong. Well, that’s not actually true. If a fever gets high enough or lasts long enough, it will kill you. Which is why hospitals work so hard to keep your fever down. A steeply inverted yield curve that goes on long enough is like having 108° fever. Both banks and shadow lenders go upside down on their “book” and stop making loans. That can freeze the economy and makes a garden-variety recession even worse. Which is why any central bank facing that scenario lowers rates and fights the yield curve.”

Curve from article:

Great info. Thanks Bikoo. I wonder if this will synchronise with the cyclical dip I’m expecting in gold into 2023 ? (like 2007/8).

NOt this time. It is not expected to have 2008-2009 style synch dip in gold with the market. The reason is ovious because financial market diverge since then.

If you read my post on yield spread vs SGR it relation with SGR has changed to positive from negative from post 2008 since 2008.

If yield curve start widening from here from narrowing SGR will move higher with the widening and market will slide for sure.

Over the years investors have experienced varieties of differing inter market relationships.

Check out my previous post on TYX yield curve vs SGR.

Here is TSI blog on 10-2yr yield spread. The charts shows this relationship works.

“Something else that affects gold’s price trend is the difference between long-term and short-term interest rates (the yield-spread, or yield curve), with a rising yield-spread (‘steepening’ yield curve) being bullish for gold and a falling yield-spread (flattening yield curve) being bearish.”

http://tsi-blog.com/2017/04/are-rising-nominal-interest-rates-bullish-or-bearish-for-gold/

Below is my post from march 12 2018.

https://goldtadise.com/?p=425966