Mining and forex

Lots of investors think they are safe in locations like West-Africa, Australia, Canada, Brazil, but they should not forget that if the gold price rises like it did from 2000 to 2008/2011, the US$ will fall and this should negatively impact producers in non US$ countries as the input costs like labour and some infrastructure will increase. Fuel and consumables that are priced in USD should be stable although. This is significant as labour is typically 30-50% of mining costs.

We clearly can see on the charts of gold price in several non-USD countries that the bull market in gold only started from 2005.

This is especially the case for Euro and Euro linked countries as the gold price in Euro only started to go up after 2005!

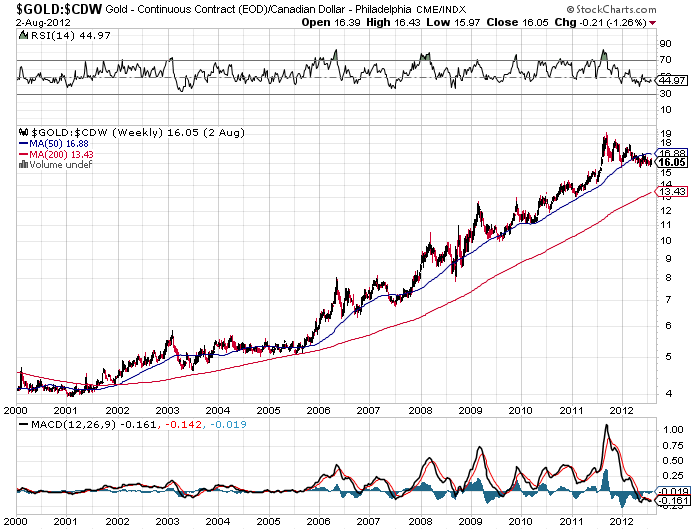

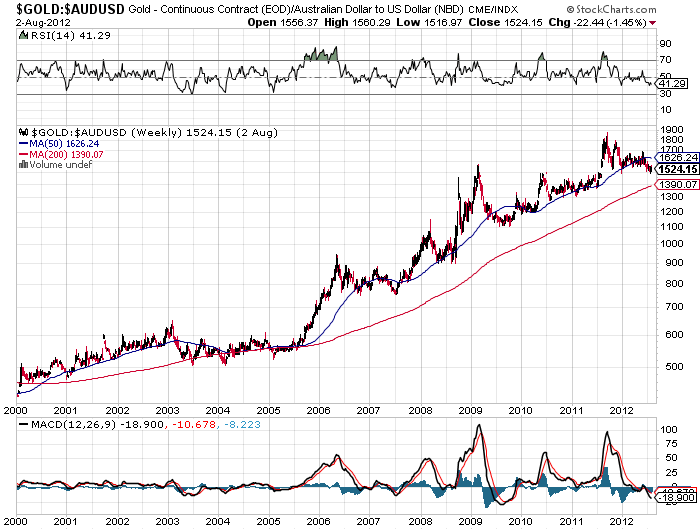

We can draw the same chart for several other countries like Canada and Australia

For the Canadian $, it was different than the Euro, as the currency only started to outperform from 2003 but nevertheless the difference is significant compared with the gold price in US$

The same applies for Australia, where the AUD started to outperform from 2002 onward, but only till 2008 due to the financial crisis, this is the same behavior as the Euro, but here the effect is worse as the AUD outperformed strongly in 2003/2004

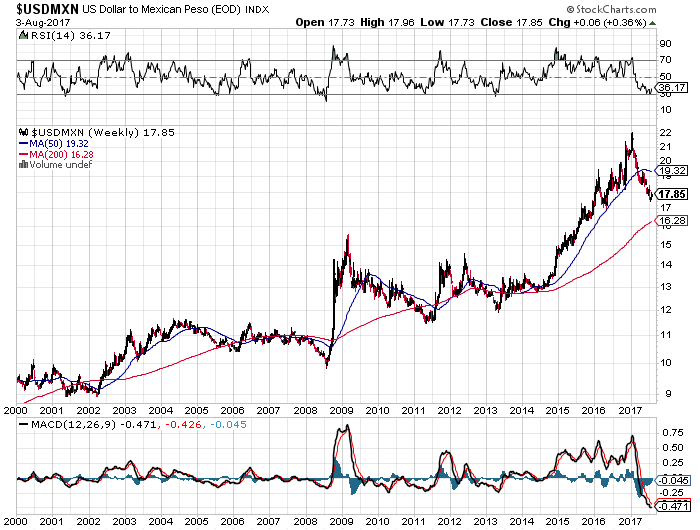

For Mexico, I just show the MXN chart and here it is far less obvious as this is a less stable country I guess, although investors should not disregard forex movement.

Another currency is the Chilean peso:

Here the effect is less or more the same, but in the LT, investors are better off in Chile as the currency is more or less stable

In terms of numbers we have the following outperformance :

Gold: up from 250- 1000$ (300%)

Euro: up from 0.85 to 1.6 (100%)

AUD: up from 0.5 to 0.95 (90%)

CDW: up from 0.62 1.1 (78%)

CLP: from 500 to 525: almost no change!

MXN: down from 9 to 11: this is the winner!

If we look at currency movements from 2008 till the 2011 gold price top, then the only loser is the USD and it is clearly a winning strategy to have gold in non-USD countries, physical or in mining assets

We can do the same for other countries, and depending on the stability of the countries results will be more in line with AUD/Eur or the MXN

This is from a website specialized in calculating mining costs:

Besides grades and process recoveries, production costs have the highest sensitivity to changes in exchange rates, with a 10% strengthening of the dollar giving rise to a $47/oz fall in average production costs on a global average basis. Exchange rates are usually the largest single determinant of year-on-year global average production cost changes. With regard to input costs, labour is by far the most sensitive cost component, by virtue of its large proportion of a typical operating cost base.

Conclusion: when investing in a company, look for value, and invest in low cost producers, and avoid strong currency countries!

Looking at recent results of EXK and AG, AISC costs are up strongly due to adversely currency movements, so even in Mexico it is not always easy.

Excellent work Alex

Thanks

Great thanks Alex. Add to this the geographical political problems as we have seen with a number of producers in Africa recently, and it is not easy to pick the winners.

Nicely done. Thanks Alex.