Canadian miners vs ROW: 0-4

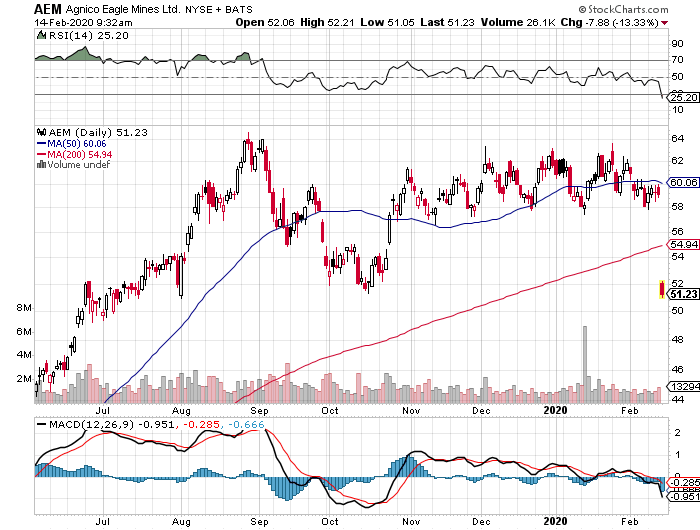

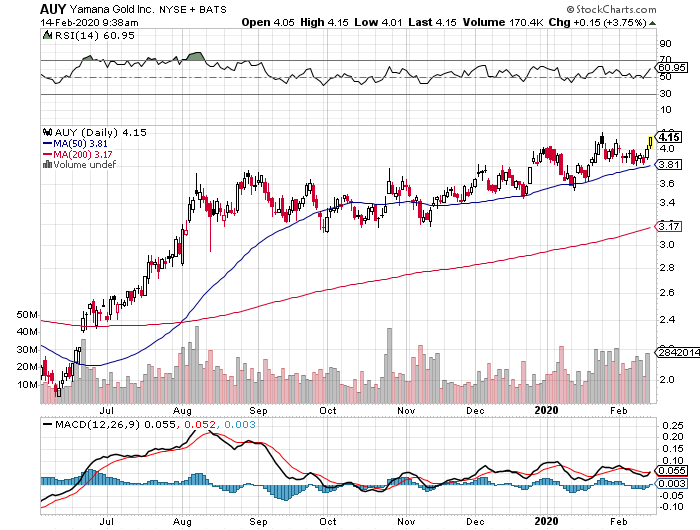

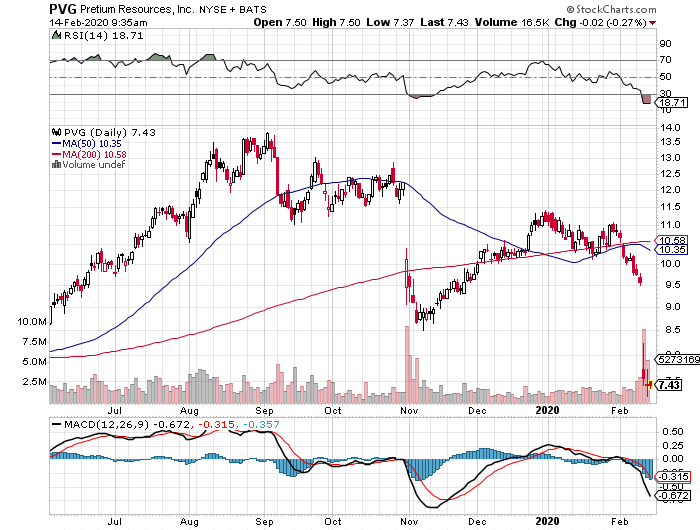

2 more big gold companies came out with earnings yesterday, AUY positive, AEM quite negative. Despite the high Canadian gold price this is the third Canadian gold company (after PVG and NGD) missing expectations. Lots of investors will be surprised I believe and it only shows how difficult gold mining is in Canada. Have no clue why exactly, is it that difficult to find skilled people to operate a mine up there? Anyhow this only shows we are still early in this possible gold bull market and majors will not expand production anytime soon or acquire explorers at crazy prices. AEM is even negotiating with royalty holders on Malartic mine to reduce part of royalty or it will not expand mine. Clearly show how tough it is to operate underground mines in Canada.

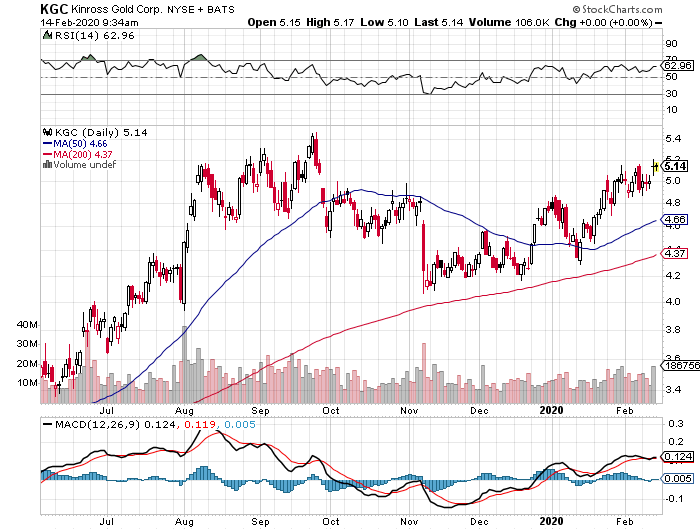

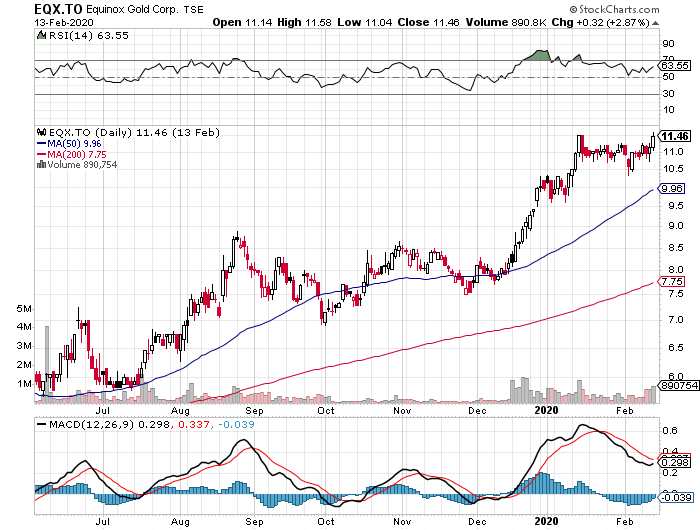

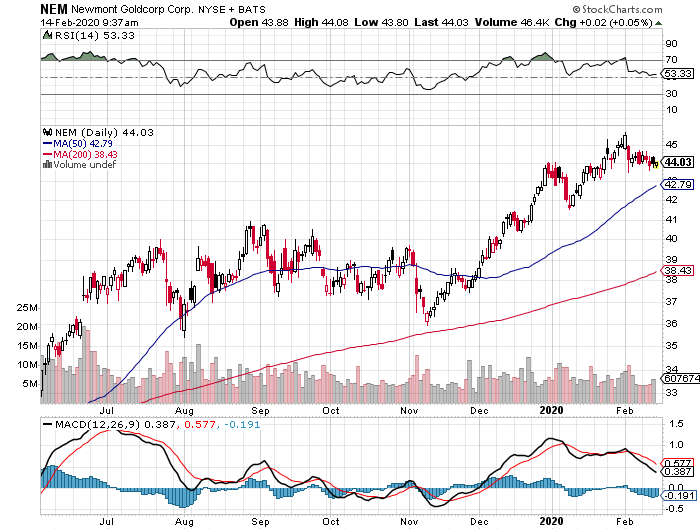

Going forward I believe it will be better to hold big diversified players with operations in several countries, including some riskier places like Africa and Latam. Both GOLD and NEM are doing well and other names like KGC, AUY, BTG, AU, … are performing in line too. Of the newer players EQX is doing quite well thanks to its no premium merger with LMC.

I guess this will be the new trend in gold mining, merger without premium and focus on easy assets with low costs and long mine life, preferably not in high cost places like Canada.

Longer term this difficult environment can only have a positive effect on the gold price as production will not increase anytime soon. Maybe holding physical gold is not such a bad choice after all.

The drop in AEM today seems excessive. They met profit expectations, and raised the dividend by 14%. They reduced 2020 guidance by about 4% due to a slower ramp up at their new mine, and apparently making some improvements at the Laronde project. AEM has had some mine failures in the past so maybe they are taking a more conservative construction and maintenance approach to all of their mines, which is not necessarily a bad thing. Longer term guidance for the next two years, however, remained steady. They are actually growing production in the intermediate term to 2.1 million ounces by 2022. The Malartic mine is 50% owned by Yamana, but AUY shares are doing fine, so I don’t think this has much to do with price action today. Market seems to be using this guidance as an excuse to take some of the premium out of this stock in my view.

I agree drop is excessive, but AEM costs have increased substantially from last quarter. If AEM can show improvements the next quarters, share price should recover, if not AEM will trade at lower multiple due to higher costs structure.

Equinox is a beauty!