Expect the Unexpected

Now what if I used my contango/backwardation analysis on Fed Fund Rates? Might be getting close to what CME does with it’s fancy calculations I look at!

We are at an interesting point, where the “fuel reserve” for a precious metals bull run is back filling, as markets are pricing in possible rate hikes!

What is kinda scary is 4 months before the Oct 2008 crash, the market was expecting rate hikes! Yikes.. talk about being blind sided… that’s about the leeway we have… 4 months.

Hopefully… a strong correction in US equities will be sufficient to flip.. and not a crash that can bring down the commodities with them!

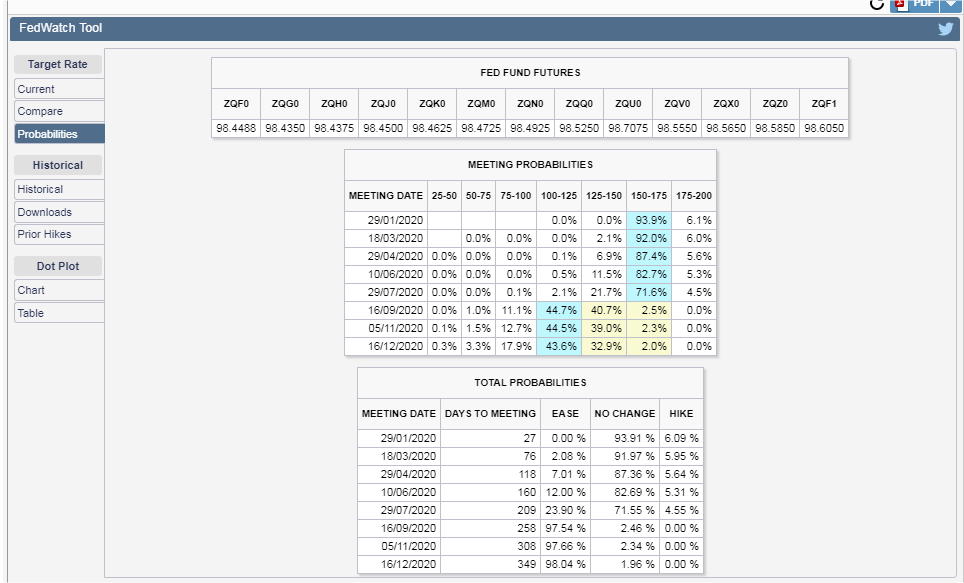

Edit: Adding CME print grabs of something strange.. glitch? https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

Check out July FOMC meeting… 21.7% chance of cut to 125-150… and 71.6% chance to stay at current level

Now check out Septembre FOMC meeting … drum roll please …. almost no chance of staying at current.. and 40.7% to be at 125-150 and 44.7% at 100-125!

WTH????

Edit: I think I found the error… when I check on tradingview.com… the sept contrat is 98.549… not 98.7075.. so I guess it’s an error in their data source

Thanks great post.

There is another warning sign in credit market. Spread between Libor 3 and 3 months treasury bill.

The spread is inching higher. But not at any critical level.

old post on the subject:

https://goldtadise.com/?p=437136

Happy New Year!!

Thanks Bikoo! New years greetings to you too!