KL buying Detour gold: down big!

Nobody saw this coming I guess, everybody thought KL would buy a high grade play like Osisko, TMAC or Pretium. Guess not, KL prefers cheaper low grade, long life asset Detour.

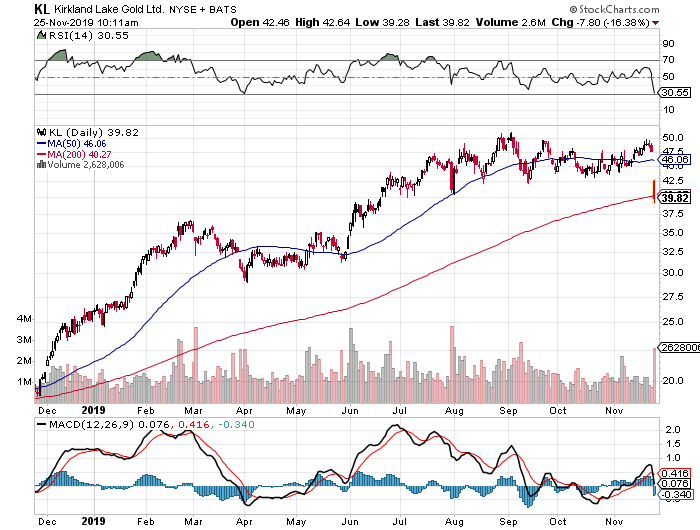

Meanwhile, the market does not like the deal as KL is adding a VERY high cost mine, KL is down 16% losing 1.6 Bn$ in market value, almost 60% of DGC value

Positive Broker comments as KL is paying DGC with expensive KL paper

KL makes a bid for Detour

We are maintaining our BUY rating and C$67.00 target price for Kirkland Lake Gold

following the announcement that they have entered into a definitive agreement whereby

Kirkland Lake Gold will acquire all of the issued and outstanding securities of Detour

Gold

Terms of the transaction:

• All share deal, 29% premium

• Total consideration of C$4.9B or C$27.50/sh for DGC shares

• Pro forma ownership 73% KL and 27% DGC

• Break fee of US$148M payable to KL and US$202M to Detour

Detour Lake is an open pit operation located in Northeastern Ontario, approximately

300km northeast of Timmins. Detour acquired the property in January 2007 and

commenced gold production in February 2013. The operation has a mine life of

approximately 22 years with an average gold production of 659koz/a with 2019

guidance of 590-605koz and $1,100-$1,175/oz all in sustaining costs (AISC).

Our take:

• Accretive on NAV (~23%), KL is trading at 1.70x P/NAV and Detour is trading at 0.69x

• EV/EBITDA modestly increases by ~3-4% on our numbers.

• Increase KL’s production profile to ~1.5Moz/a.

• Pro forma reserve base of 21.2Moz based on year-end 2018 numbers.

• Costs will increase considerably, DGC 2019 AISC guidance ~$1,200/oz vs. KL 2019

AISC guidance of $560/oz, so we calculate a blended AISC on 2019 numbers of ~US

$750-800/oz, a ~34% increase.

• This is off script for Kirkland Lake which operates two of the highest margin assets in

Macassa and Fosterville.

• The company claims US$75-100M in synergies though we question where this will

come from. The Detour mine site is located several hundred kilometers from Kirkland

Lake’s Macassa operation.

• This deal could get the M&A space moving. Other single asset producers in Canada

with potential for M&A activity include Pretium Resources (PVG: TSX; C$12.49 | SPEC

BUY | C$18.00, Kevin Mackenzie), TMAC Resources (TMR: TSX; C$3/42 | SPEC BUY |

C$7.50) and Wesdome Gold Mines (WDO: TSX; C$8.25 | BUY | C$9.00).

Valuation: Kirkland Lake trades at a premium to peers at 1.70x P/NAV vs. 1.03x, and

9.9x EV/EBITDA vs. 8.5x. We believe this premium is warranted given the company’s

assets in low-risk jurisdictions and high-grade ore, which continue to help Kirkland

achieve some of the highest margins among peers.

Should have bought OSISKO…

(Disclaimers–I own KL and bought more today. I owned a ton of OSK having bought it for pennies as Oban — one of my few successes in recent years — and sold it a couple of months ago. But I am an extreme amateur and am just guessing my way around in the mutterings below).

From what I understand an OSK purchase would have been tough. KL at least in the recent past was heavily influenced by Eric Sprott and may still be. OSK on the other hand is a Sean Roosen company. I saw written musings about whether the two would actually be able to negotiate nicely over OSK, implying that probably not, even though there otherwise might have been pluses to the idea. I strongly suspect Roosen either wants to run OSK himself or will hold out for an exceptionally good deal. I don’t think Roosen is desperate at all, and unlike the management of Detour I don’t know that he’s had forceful shareholder pressure to change.

With Detour there has been plenty of turmoil at the top. Big shareholders have pushed for and gotten some change because of perceptions of inefficient and bloated management, but despite some changes following a proxy fight I think there has still been grumbling. Makuch, CEO and President of KL, on the other hand, I believe has the reputation of being smart. I have read assertions that he might also have at least mild tendencies towards being be a control freak (maybe freak is too strong a word). Thus there is at least the possibility that a large inefficient operation but with many years ahead of it gets put in better order. Big shareholders from both institutions may like the idea. Big institutions for better or worse may tend to like to hold really large companies, and now KL will be larger. Makuch at least for a while may have a halo over his head in the eyes of some institutions. KL will (if the gold price holds up and mining expenses don’t get too high) have one more long-term revenue source. It will be more diversified in the type of mines it holds, but not much more scattered geographically than it is now. Thus it will look as if it is transforming itself qualitatively not just quantitatively. If it successfully digests this acquisition without going crazy then it looks super for institutional money managers who have to buy something relatively large with a good reputation. It will probably check boxes as a “growth stock” as well as a precious metal company.