Gold companies: cheap or not and when to sell

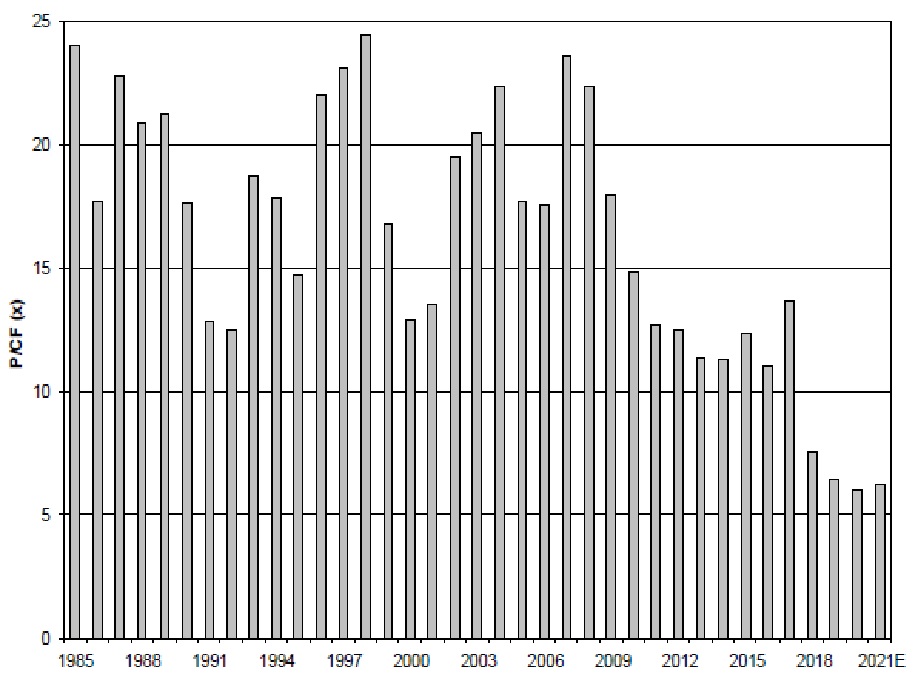

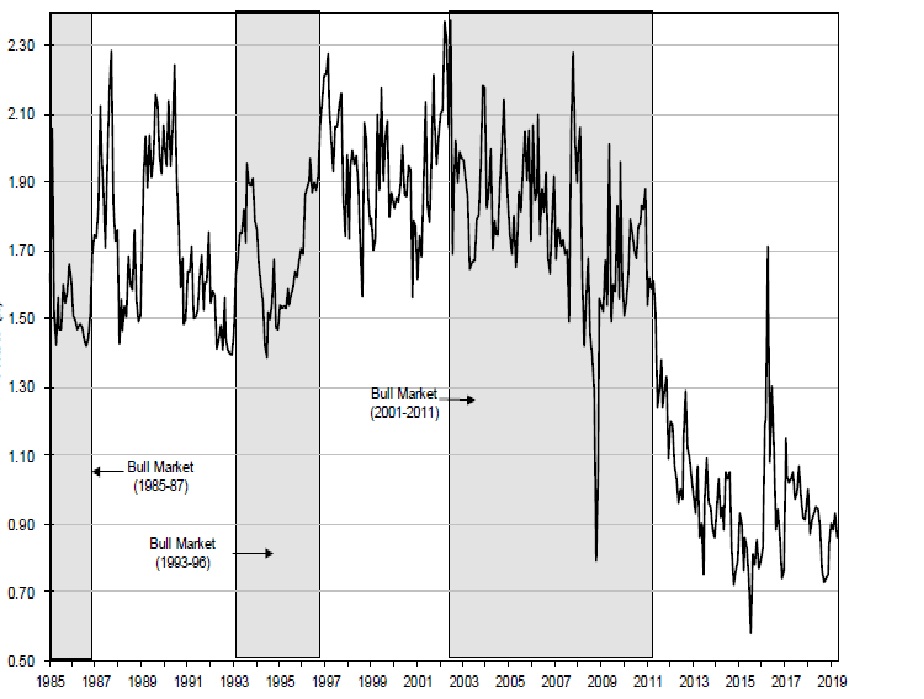

It looks like the valuation of gold miners never has been so cheap, especially looking at P/CF multiples gold miners are undervalued, less so looking at NAV multiples however.

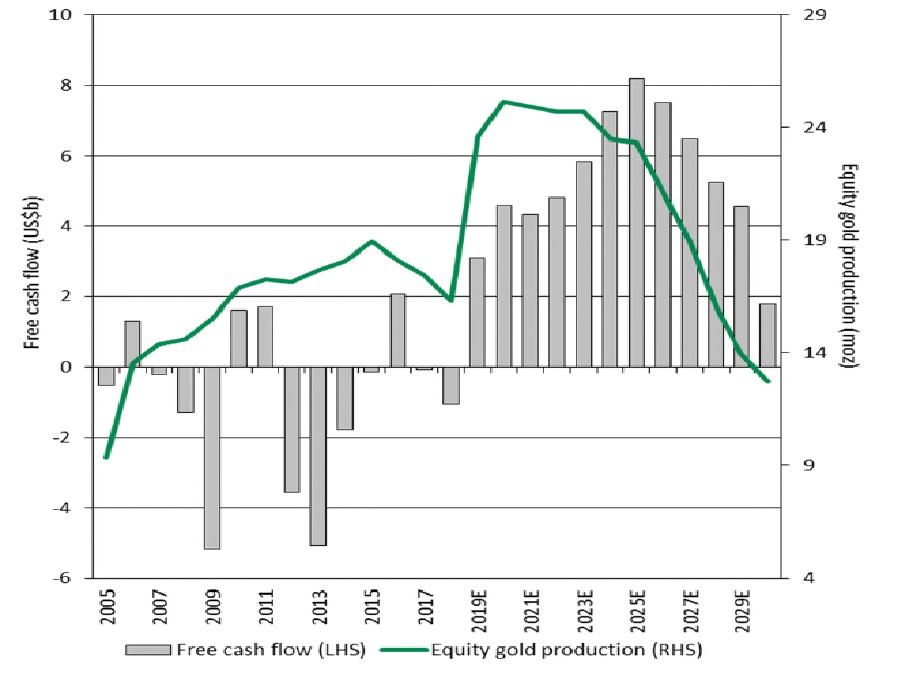

If we look at the long term, we can clearly see that due to under investment in exploration and falling grades, production will decline strongly from 2024 onward and free cash flow will be 60-70% lower in 2029 than its 2021 top level.

Conclusion: valuation of miners is clearly on the cheap side. Main reason is not only the lower gold price, but mismanagement of companies and falling grade play big part of it too.

Longer term you better own the real stuff as the declining gold production should impact gold price positively (If forecasts are correct) and miners profits negatively. Better sell all your miners ahead of forecasted 2025 top in free cash flow.

Great stuff.

Do you have the original source of those? I’d love to include them in my book.

Alex is da man Jordan

He knows the Miners Fundamentals

🙂

https://www.merkinvestments.com/downloads/2019-05-16-merk-ASA-webinar.pdf