Gold Fundamentals

I’ve read his blog for several years, a mixture of fundamental and technical analysis sometimes referred to as “Technimental”. Regardless, Steve Saville has been on the right side of the major markets (equities, bonds, precious metals, etc.) during that time. He’s repeatedly maintained that gold is not in a bull market while the S & P 500 is. https://www.speculative-investor.com/new/subscribe.html

He kindly gave me permission to post this section of his most recent newsletter here:

Gold

The Fundamentals

“When most market analysts state whether the fundamental backdrop is bullish or bearish for gold, they are stating their opinion and their opinion is most likely based on gut feel. They have no way of objectively quantifying the fundamental situation. Instead, they look around and come to a conclusion based on what they see.

The most obvious problem with this approach is that any conclusions will be strongly influenced by personal biases. Another problem is that the fundamental drivers of the gold price aren’t statistics such as the money supply and the amount of government debt, but the general PERCEPTIONS of what these statistics mean for economic growth, the financial system, “inflation” and interest rates in the future.

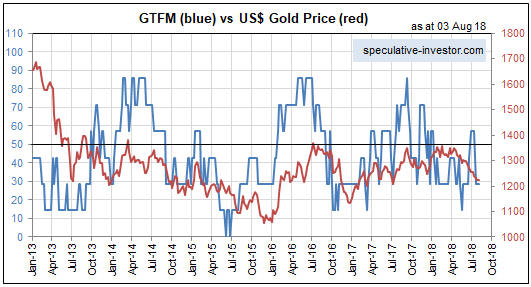

Our Gold True Fundamentals Model (GTFM) is not influenced by our personal biases. The Model’s output is what it is, regardless of what we think of the economic and financial-market situations. Also, the Model’s inputs are largely based on how market participants collectively view the economic and financial-market situations. For example, we may very well think that the economy is ‘skating on thin ice’, but if credit spreads are very narrow then we know that our view is an outlier and that economic perceptions are not supportive of the gold price.

When constructing the GTFM we considered — based on the general idea that gold’s value is the reciprocal of confidence in the financial system and the economy — what should be the main influences on the gold price. This gave us a list of potential price drivers. We then tested each of these potential drivers against the price data to confirm that there was a significant correlation. For example, it can be shown that there is a strong and consistent relationship between the TIPS yield and the US$ gold price and between credit spreads and the US$ gold price, but no consistent relationship between the US$ gold price and either the CPI or the level of federal government debt. The result was a list of seven factors whose inclusion in a gold model was justified both logically and empirically.

The GTFM is sensitive to shifts in the fundamental backdrop. This makes it quick to signal significant new trends, but also makes it susceptible to being ‘whipsawed’. For example, it got whipsawed between late-June and mid-July of this year when it went from bearish to bullish and back to bearish. It will continue to get whipsawed from time to time, but over the past 15 years the intermediate-term trends in the gold price have always been consistent with where the GTFM has spent the bulk of its time.

The GTFM remained in bearish territory last week.

In the short term, the most likely cause of a positive shift (from gold’s perspective) in the fundamental backdrop is a T-Bond rally combined with a decline of at least a few percent in the S&P500 Index. However, looking beyond the next few months we can envisage a very gold-bullish fundamental backdrop emerging on the back of rising US inflation expectations. Rising inflation expectations are bullish for gold to the extent that they reduce real interest rates, steepen the yield curve and weaken the US$.

A substantial rise in inflation expectations probably won’t be a factor in the financial markets over the remainder of this year, but it could be the most important factor during 2019-2020.”

The ‘GTFM’ model goes up when gold price goes up, and down when gold price goes down. No shit Sherlock. As a predictive tool, it’s about as much use as a chocolate teapot. I would suggest cycle theory can tell you when price will be going up, and when it will be going down, not just in the medium term, but years into the future.

Thanks for the kind words.

Of course it does, and that’s why I’m primarily a technical trader/investor who [almost] always appreciates your posts.

But it does have some usefulness in showing whether or not conditions favor a bull market environment or not, and that can temper expectations as to whether or not a rally means the beginning of a “new bull market”.

He also had some far better work that he would not allow me to post. I’ll attempt to fill in that with my own work in another post.

Hi BBM. Apologies. I didn’t mean to be offensive. I was just being flippant. All I really meant is that there are numerous indicators that move up and down in tandem with gold price. What’s useful is having a predictive tool.

No problem, Northstar.

What I’d look for with his model is persistently high readings that remain above 50 on that chart for AT LEAST 12 to 15 months. THAT would be of some predictive value to me. Until then overbought rallies into resistance are likely sells. In other words, a sideways market where the major downtrend from 2011-12 might resume with a vengeance unless the US Dollar resumes its downtrend first.

I think you’re right to point out that the dollar is key at the moment.

Good grief I remember reading Steve Saville way back , maybe 2002?

Hope he is right. I’m looking for more bear action.

I did have an USA CPI inflation model based on oil/energy action that I lost interest in so I didn’t pursue it any further.

It worked very well in 2014-2017. I had concluded that if it stopped working then inflation would take off in whatever direction the deviation from the model indicated.

I need to look at that again, perhaps – but I can’t really be bothered.