I’m accumulating Ascendant Resources. ASND.TO ASDRF

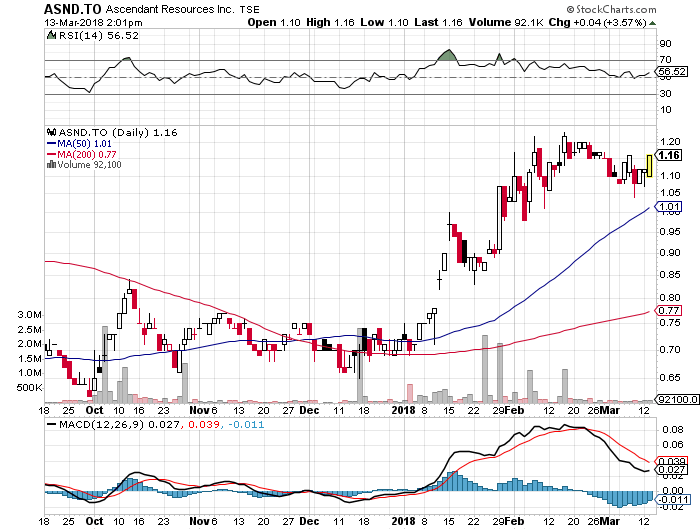

This is an extremely under the radar play. Ascendant bought the El Mochito Zinc mine in Honduras for peanuts and rehabbed it. The company is guiding 32-40mln EBITDA and 14-20mln Free Cash Flow for 2018 at 1.50 Zinc and 1.10 Lead. The enterprise value is 57mln US. Do you guys have any idea how cheap a company is that is doing 40mln EBITDA with a 57mln US enterprise value? They can basically buy back the entire value of the company in 16 months. You never see things this cheap. WHat gives me more confidence is that Renaud Adams recently joined the board and bought stock. He is the CEO who turned around Richmont Mines and turned it into a 4 bagger on the eventual sale to AGI. This is a mine optimization play and he is a mine optimization guy. Steve Laciak of Dundee securities has been going crazy on this name and been buying 1 million sare blocks. His last purchase was 1.17 CAD. He owns 16+ percent so the float is small. The last time he went nuts on a company it was bought for a 79 percent premium roughly a month later. We are about 6 weeks in since he announced he started buying in a PR. I think that this happens again. Small float and barely trades on the US side so be careful. I have a 1.13 CAD average full disclosure. It’s difficult to buy stock unless you pay up for it.

I’m watching this one but haven’t bought yet. Another Zinc play you may be interested in is Rathdowney Resources. It’s quietly moving ahead, but not much reaction in the share price.

I will give it a look thanks.

Thanks, Cashcosts, I always appreciate your recommendations.

Cashcosts,

This is intriguing, for sure. Curious, what do you see as the downside risk? What could go wrong? Thanks!