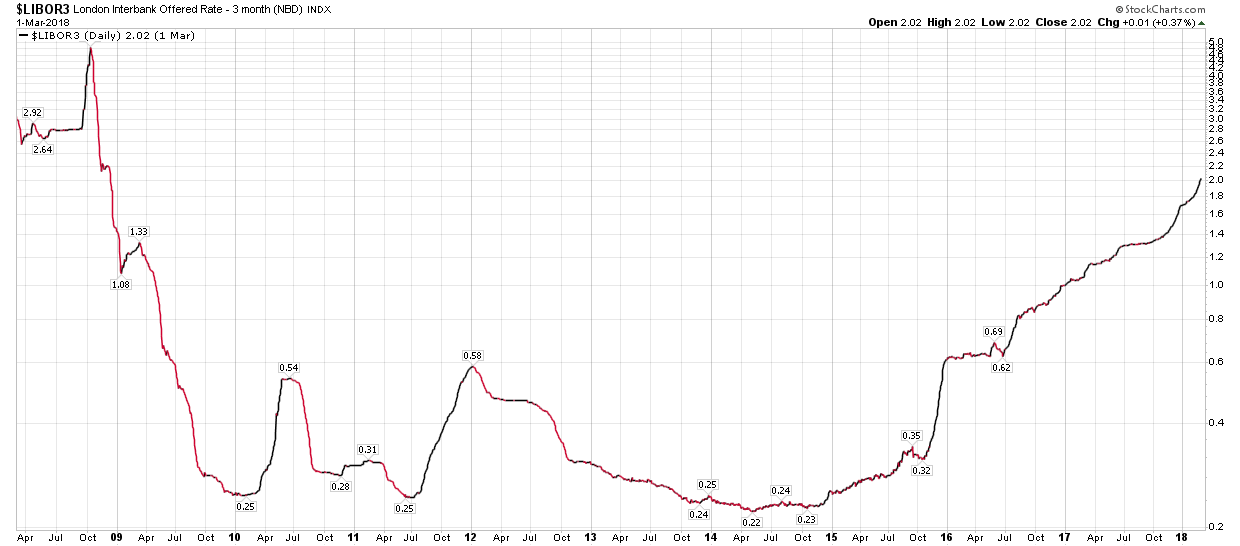

LIBOR

In 2008-2009 market crash 3 month LIBOR was at 5.0. Now it is heading straight up.

Telegraph:

“Libor surge is nearing danger level for debt-drenched world”

“The stress signals of the global credit system are flashing amber. The offshore dollar funding markets that lubricate world finance are facing an incipient squeeze.

The “Libor-OIS spread’ – watched carefully by traders – has risen to levels reached during the onset of the Chinese currency crisis in early 2016, and during the onset of the Italian and Spanish funding crisis in late 2011.

The three-month rate for dollar Libor (London Interbank Offered Rate) used to price a vast nexus of financial contracts around the world has spiked to a 10-year high of 2pc this week. A third of all US business loans are linked to Libor, as are most student loans, and 90pc of the leverage loan market.”

LIBOR chart:

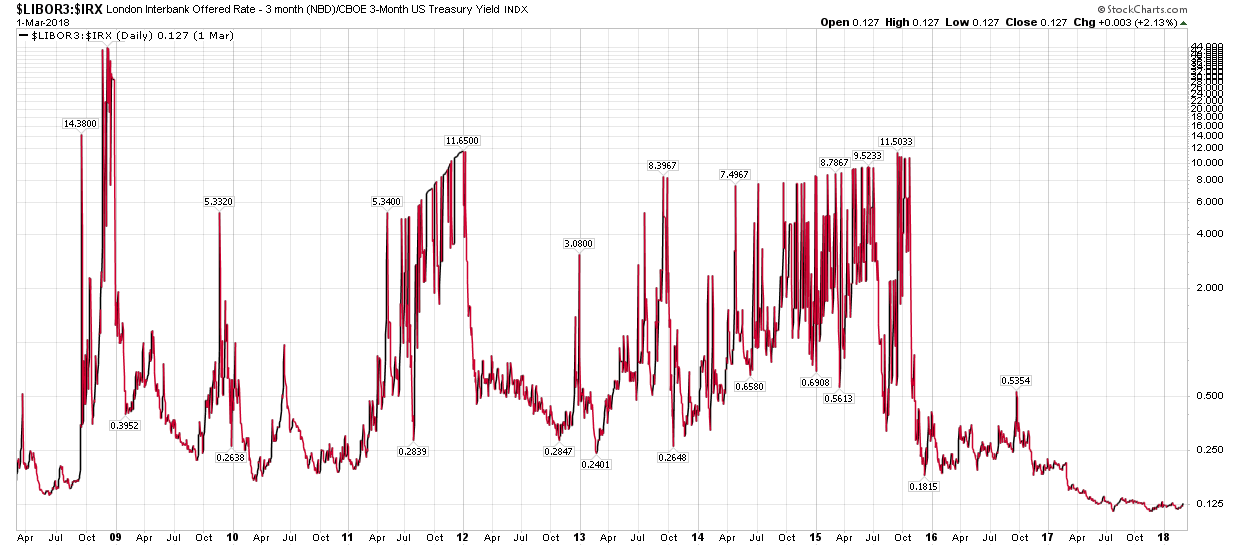

A breakout of the ratio LIBOR to 3 month T bill will be a warning for the market similar to 2008-2009.

On the LIBOR monthly bar charts, both 1m & 3m, there’s a large gap in late 2008 that was never filled.

At a minimum, I expect both gaps will be.

Also, FWIW, I’m not sure whether TA is of much, if any, use in determining the future price of LIBOR

given that LIBOR is effectively a measure of banking system risk.

Who ever knows about banking system can shed some light on how LIBOR and 3 months T bill rate come in to play. If ratio breaks out to upward, what is the implication on bank borrowing and capitalization.