interbank lending…..??

Is anyone following this? Interbank lending stats discontinued at FRED?

Most curious thing – if they discontinued on 1/3/18 per FRED site, why is it just now (today) getting serious attention? – earliest screen shot I could find of was 02/08/18 at Seekingalpha – a casual mention.

A hoax? Direct links below.

https://fred.stlouisfed.org/search?st=interbank+loans

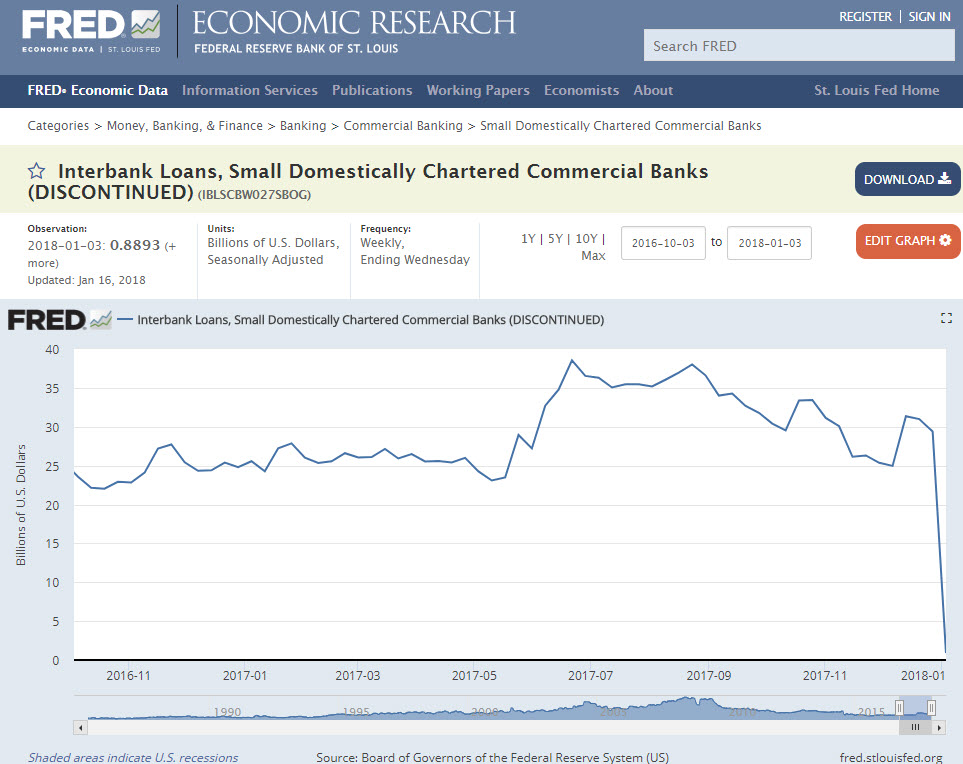

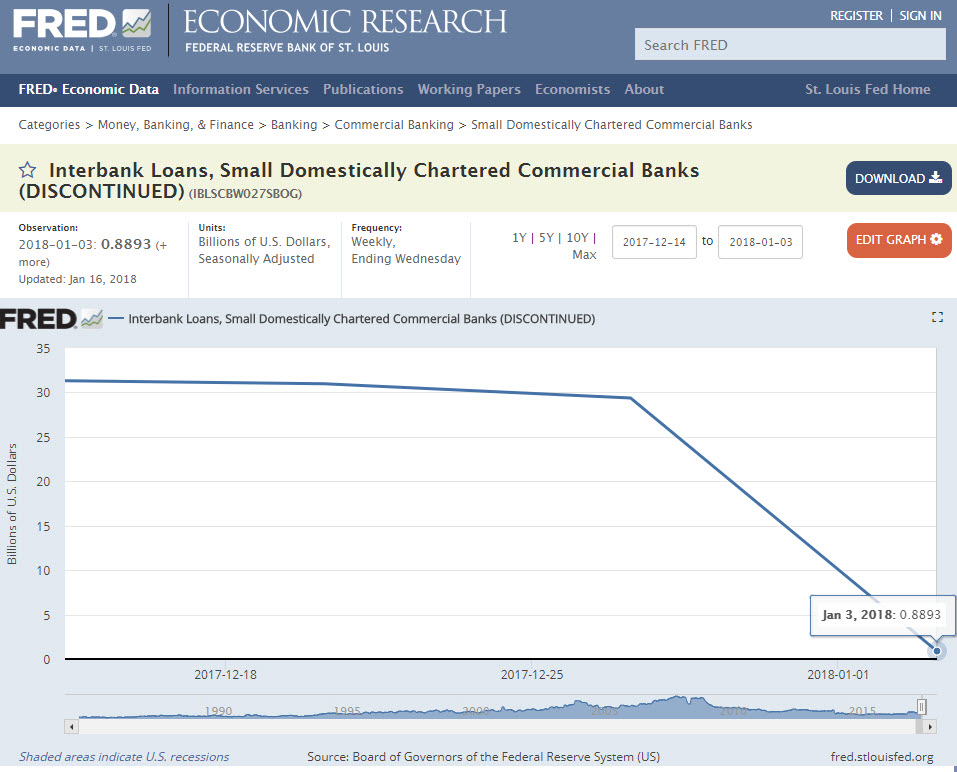

https://fred.stlouisfed.org/series/IBLSCBW027SBOG

On 4chan…. of course YMMV as far as truthiness there but including just the same…..

http://boards.4chan.org/pol/thread/160311413/warning-this-is-not-a-drill

Another article on ZH

https://www.zerohedge.com/news/2018-02-13/plunge-interbank-lending-straw-broke-feds-back

There’s a screenshot in this link from Feb 8th.

https://seekingalpha.com/article/4144946-major-pattern-shift-occurring-bond-market

Thought I’d share…GTLA.

https://socioecohistory.wordpress.com/2018/02/09/lynette-zang-the-market-is-in-trouble-are-you/

this is where I first caught wind of it, hmmmmm odd to say the least. Discontinue until the reset perhaps….

Thanks – for anyone following, jump to 14:05 in the vid for her analysis where she discusses’ the FRED charts above.

As someone in the ZH forum pointed out – advance notice of the action was posted at FRED 1/12 but doesn’t mean it’s removal as an entire category isn’t important or telling (of what??).

https://www.federalreserve.gov/feeds/h8.html

January 12, 2018

Changes to Items Reported on the H.8 Release as of January 3, 2018

Effective with this release, several changes have been made to the line items shown on the H.8 release. These changes relate to the Federal Reserve Board’s notice published in the Federal Register, 82 FR 49207 on October 24, 2017.

The following line item changes have been made on the release:

1. Previous line item 26, Fed funds and reverse RPs with nonbanks…….. with nonbanks and the category Interbank loans (former line item 31) has been eliminated.

This drop was in a previous post by some one else. My ? is why there is not change in LIBOR?

Only other reason could be that Banks do not want to be stuck with debt. OR they have drop in business activities.

YYZ: like to PM with you. What is your e-mail regarding legend removal????

Must have missed that prior post (I read Graddhy’s last post back when it had 3 comments and in three days it explodes – guess I need to visit more often). I am ready to take action with TD (submitting cert and their forms + $) just haven’t got around to it yet – I might hit another roadblock but as of right now things appear green. I’ll PM you.

Here’s my hairbrained idea on what’s happening, having followed the ’08 crisis resolution’s effect on domestic currency markets:

CB’s ultimate goal is to corral as much of USD M2 as possible so that rate changes (which no longer require a courtesy 2 week notice but can be effective immediately – fed rule change a year or two after the ’08 crisis), affects as much USD currency as possible – basically a mass currency value control mechanism.

Gone are the market rate setters of huge amounts of M2 – labeled by the US Treasury as the SHADOW BANKING sector – the false flag under which control is being assumed.

1) Non-Gov’t MMKT Mutual funds have nearly dissapeared – they now deal in gov’t debt/MBS (Fannie Freddie, possibly Sallie (gov’t student debt – yea right…) etc. at least the ones that have survived and wanted to avoid ‘Gating’ and forced into breaking-of-the-buck floating navs << MF companies fought tooth and nail against they but lost against the treasury secretary – now all $1 nav MF MMKT's hold ONLY Gov't securities.

2) Kill the Commercial Paper market – effectively done via #1 above

3) The latest – kill inter bank lending such that the FED is now nearly 100% in control of the price of currency dealt to/from banks – at least SHORT term which they hope can wag to some degree longer term rates (the dog).

ST Treasuries used to serve as a base (riskless) rate and Commercial Paper, MMKT MF's and the Prime rate floated somewhat above that – depending on creditworthyness etc – as determined by the market. NOW – those are nearly all gone – it's Gov't paper "guaranteed" at USD $1 per unit OR non-gov't paper – no guarantee of future value.

This seems to me like Central Banking command and control 101. Are we being set up for a negative interest rate environment (or effectively such through other means) when the first 175bp reduction doesn't do the JOB? Typically the fed requires 400bp's to recover from a recession but no room for that now.