Silver stocks or ETF?

In order to play the possible big outperformance of silver vs gold the next 2/3 years it is important to be positioned in the right silver plays.

I personally believe a lot of mid cap producers like EXK, GPL, and even AG are to avoid. Why? Increasing cash cost + increasing capex as these companies under invested in sustained mine development during the downturn from 2010-2016. Going forward these companies will have it difficult to post significant free cash flow with silver at 25+ level in the future.

I therefore believe it is better to buy names like PAAS, CDE, HOC.l to name a few bigger producers.

Of course one can always to choose to buy the SIL or SILJ ETF. I personally believe the SILJ is not a bad choice if you choose for the bigger silver names.

Of course the better alternative is to buy explorers, as all the issues of capex and free cash flow are not present here!

I like names like SSV, MGG, AXU, DV, BCM, KTN and BBB, just to name a few. SSV is a nice company , but they only have 40% of their deposit. DEF is an interesting play too, but they have few ounces proven yet. MGG, is said to be the next MAG silver, but is not very cheap anymore. BCM has a very significant asset in Peru, I like the company, but favor others that are less known or in better locations.

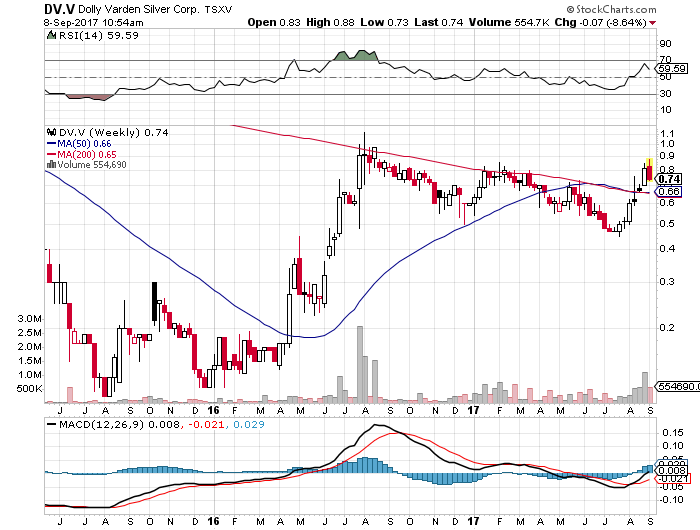

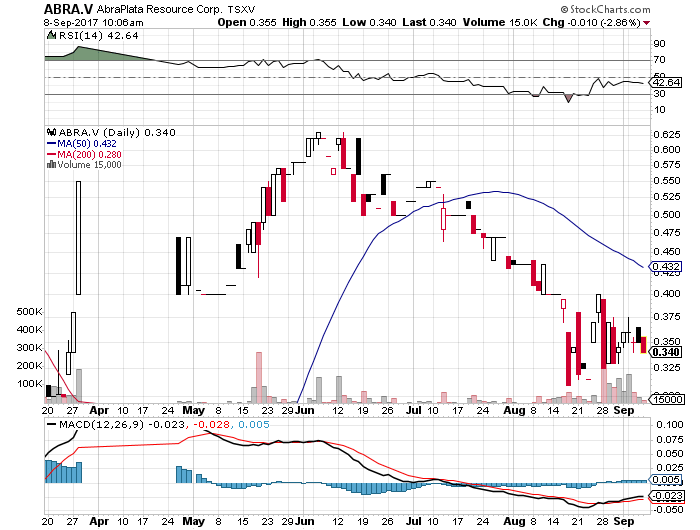

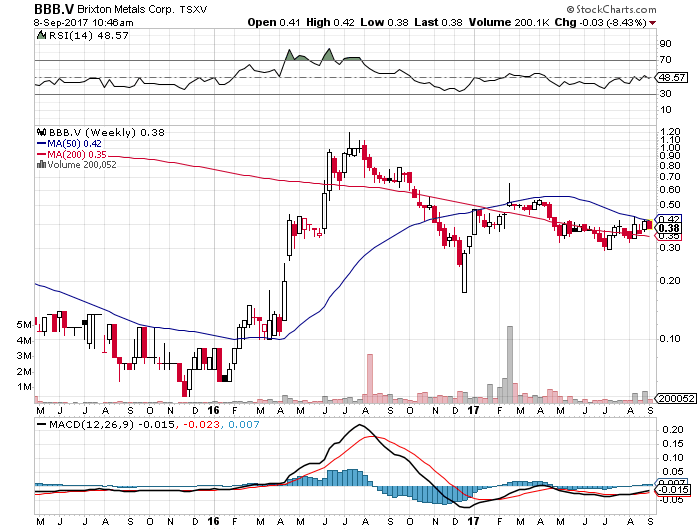

My favorites are DV, ABRA and BBB. DV has a high grade silver deposit in BC, with Hecla as partner. I am sure this company will not be around in 24 months with these grades, the same can be said of ABRA (Argentina), although here it is a different story as the market is waiting for PEA publication and BBB (more speculative) could be the next AXU if they define a significant resource of high grade silver in 2017/2018.

I like these 3 explorers as market Cap is very low compared with other ones and with producers. I know several investors like USA. I believe this is a nice name, but market Cap is 8-10 times higher than these explorers as it is a producing company. If you value these explorers at price/ounce these are really cheap names that could go up 3-5 times in value without silver going up a lot.

BCM is valued at 1.2$/ounce, even DEF with a market cap of only 35M is valued at 1.2$/ounce, including future ounces!

If we look at DV and ABRA, both names are very cheap. DV is only valued at 0.35$/ounce if we include future resource expansion and ABRA is even cheaper at 0.2$/ounce. BBB is more difficult to value as a lot of drilling still has to be done, but I would say 0.35$/ounce should be realistic.

I know there are several other silver explorers around, but few have significant proven ounces, low market cap and decent grade.

Thanks for this

Thanks.

dolly doing the backtest

Low risk entry at these levels as insiders are buying at 0.73.