Integra taken out

I just want to show the merit of LT investing in good mining companies with solid projects, besides trading every gold down turn.

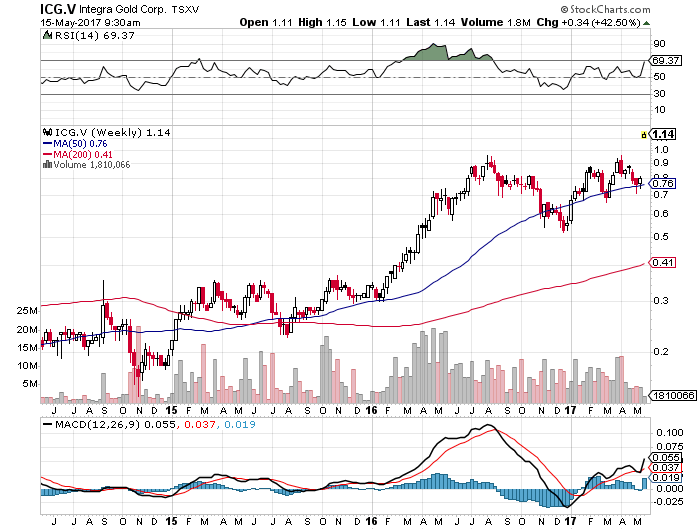

I am invested in Integra since 2015/2016 at 0.2 level and I am happy to see 500% return in 2 years. This shows that It is possible to make money from the long term holding of mining shares without trading the gold volatility.

I believe it is a good deal/fit for ELD, and may even hold part of ELD shares after take out, as I start to like this company, even with Turkey risk.

I looked at some mid Cap producers to invest my ICG shares, but see less value/opportunity here

BLK, a beaten down Australian producer, I do less like the progress of company, with lot of questions about current oxide mining plan. The same for their expansion plans as they only released a scoping study (no feasibility), and do have less knowledge to mine sulfides. Valuation although is cheap.

TGZ, very cheap producer, but shorter mine life, high cash costs, and questionable M&A, as the project they acquired from Gryphon will have double forecasted capex, lower grade and less ounces, so it makes this project far less interesting. It remains very cheap however, but at high AISC levels.

Explorers/developers on the other hand show more opportunity to create value I believe

PGM, could be another Integra, but with some development risks involved

Other names that could be acquired in the next years could be VTT, FPC, PVG, MAX, SBB, PLG,…

Of course there are many others, but difficult to find company with high IRR, low AISC , safe location and resource upside. Suggestions always welcome

Good going, Alex. I have some ICG.v too.

Congratulations Alex, thats fantastic!

It’s nice to have some gems like that. Mine is Mariana Resources – approx 400% in 18 months or so.

Indeed, Nice to have, but difficult to find.

Yes great result. I had a small holding in one of my accounts. It is these takeovers that is keeping my portfolio alive at the moment. I am sure there will be more.

I own both Mariana (I heve sold half of my position last week) and Integra.

I don’t know what to do with Integra shares,would Eldorado be a good bet for the future or it would be better to sell all the shares and invest in something new?