Spock Homerun : Anfield Nickle (ANF.V)

I showed you the value of information…Now go get it…

-Gordon Gekko to Bud Fox, Wall Street 1987

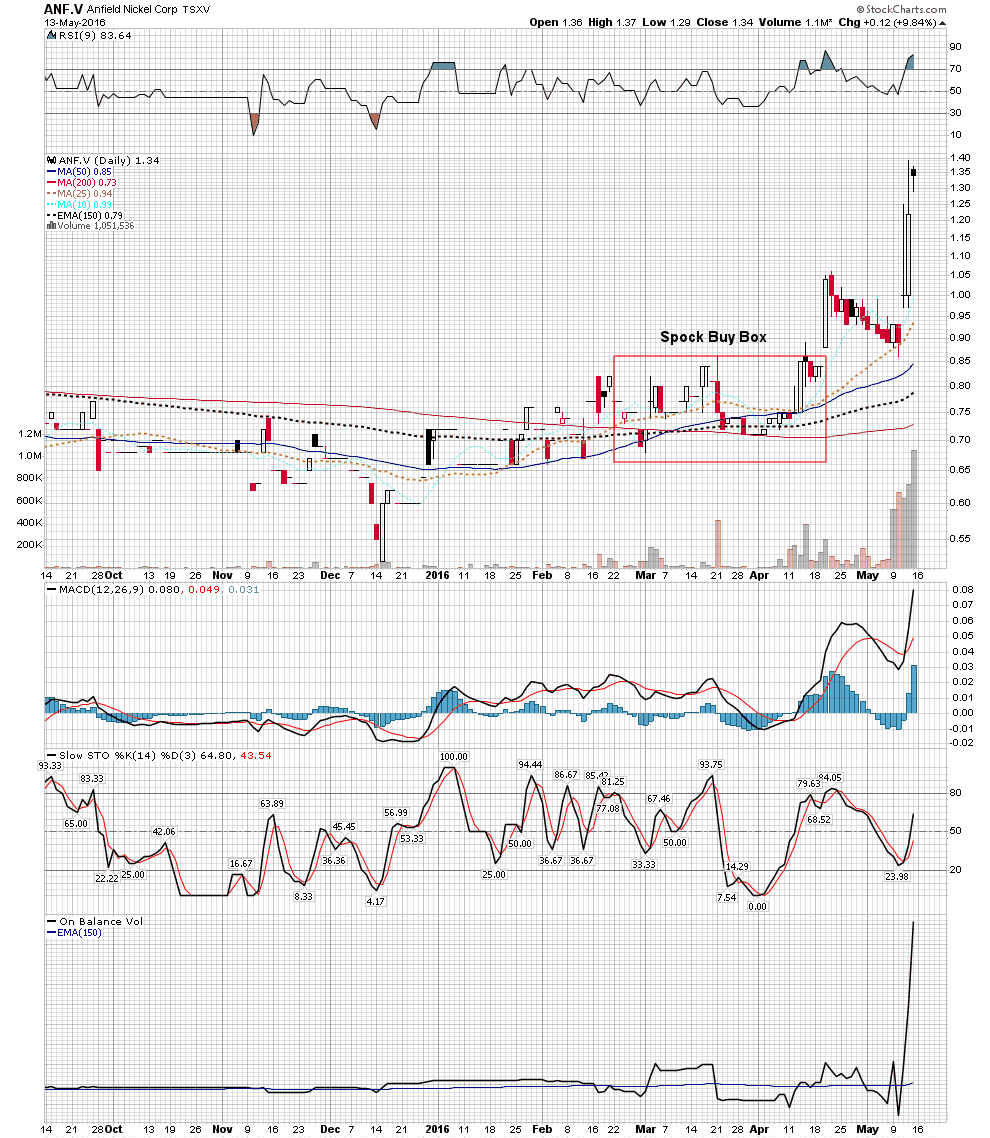

Folks this is exhibit A on the value of information. For anyone still holding out on coming over to Spock’s site

www.spockm.com

take a look at what you could have gotten buttoned down over the past month. As a team we scoped out the story of the buyout of Magellan Minerals by Anfield Nickel. We caught the scent 2 months before the market realized what was going on and took advantage of it. We held this one close to our chest. If one was not in on this deal before it launched it just left you behind and we caught the scent before the market did.

I am posting the piece I wrote up a few weeks back regarding the buy out of Magellan by Anfield and its meaning. It gave adequate time to get positioned. Once the market figured it out there was no more time. A case of “got to be in it to win it” and we were.

Here is the final post on the Anfield Nickel story:

Today I traveled to Vancouver to attend a wedding, a funeral and a near death rescue. It was an amazing day as it happened all at once and in one room. It was the shareholders meeting which approved the takeover of Magellan Minerals by Anfield Nickel. For most this had the appearance of a very boring and unattended formality, however for a value seeker I found it incredibly exciting.

First off, let me say I don’t do puff pieces. This is NOT an Icahn pumps Apple story as I am not here to sell anything. I write for two reasons, first it disciplines me to organize my thoughts and I choose to pass these writings along in order to develop relationships with other similar investors who may at some time pass along their ideas to me…period. So don’t interpret my comments as a sales job as they are just my observations as an investor who tries to have a nose for value.

If you have read my piece on the 3 phases of a bull market you know a little about how to recognize phase I and the beginning of a bull market. You fully understand its value to the investor, yet why few people ever buy there. Instead, the average investor buys Apple at $125 after Carl Icahn pumps it on Cramer’s show when he makes his call that its going to $240. He buys it for two reasons, first he gets swept up in the hype of a phase II or III and second he buys what he wishes he had bought after being attracted by the price action. What we have here in Anfield Nickel is the absolute polar opposite to this process and, by the way, this process is how one makes BIG Money.

So let’s do a visualization exercise. What if for once you had the opportunity to make money the same way using the same rules as one of the most successful, respected resource investors in the world? To get in at the absolute ground floor and under the same terms as one of the most wired-in, insiders in the industry? You have always heard how this crowd puts together deals for themselves then later issues shares at much higher levels for the muppets later down the road. But, this time the deal is to invest alongside the principle agent who owns close to 50% of the company. And to top it off, this arraignment will be done so far below the radar that no one either knows or cares about the deal. That’s the set-up arrangement, but it gets even better. Back at the top of the previous bull market investors were paying nose bleed valuations for all PM assets. They of course got destroyed in the bear market during the annihilation phase. Rather than purchasing at those levels picture yourself buying quality gold assets on the courthouse steps in a bankruptcy sale where only you show up! My friends, this is what we have delivered on a platter with Anfield Nickel. Even the name is intended to disguise the value, after all who wants nickel? And besides they don’t even have nickel anyway, they sold the last of it!

This is the definition of base level Phase I investing.

This deal is so far under the radar that I was the only shareholder that even showed up who was not a corporate officer! That’s right, out of 15 people in attendance I was the only outsider that even cared. The CEO and all the corporate officers made it a point to thank me for showing up! This was a team that has worked this asset in Brasil for the past 10 years . They have just scratched the surface drilling about 30,000 feet and defined about 950,000 Oz of high grade gold. There is lot’s more out there folks, the district has produced somewhere between 20-30 million oz. Magellan’s orebody is just what they could define with their limited budget. This is a district style play. The senior VP for Corp development described to me how the development so far is similar to how the districts in Red Lake and Timmons appeared in their early stages. Folks, let that sink in for a while and realize the potential here. After today this guy no longer has a job with this company, he has no incentive to paint a false picture.

So after today Magellan no longer exists, all corporate officers have been released, all options in the stock have been canceled. What they pass to Anfield is an orebody with known high grade that is open at depth and strike. It was a great project that simply ran out of financing and needed a rescue. It is a casualty of the worse bear market in over one hundred years. Simply put it was ripe for plucking and it got plucked.

The Focus is now on Anfield

So who is Anfield Nickel? It is a base metal exploration company which just sold all of its base metal assets for $43 million to be paid out over the next 3 years. The amount can be reduced if paid out faster, but it leaves Anfield simply as a corporate shell. So let’s dig deeper and try to figure out what they are up to. It’s not hard to figure out really, as this appears to be Ross Beaty’s mothership for conquering the gold sector in the next bull market cycle. This is huge…,why? Because we know how this man thinks and we know how forward looking and visionary he is. In the early 1990’s he started Pan American Silver. In the early 2000’s before anyone really figured out what China was going to do to the copper market he bought up shelved uneconomic copper projects when copper was 60 cents/lb when they had little value. This turned out to be a 100 bagger for him. He then developed Alterra Power as a conscious cleansing green energy company. He husbanded his resources during the great bear market of 2011-2016 and now he is rested and ready for the next bull.

The Mill

Recently Anfield bought Troy resources mill close by the Coringa project (Magellan) for $4.5 million. One of the officers of Magellan told me the replacement cost of this mill would be north of $30 million. It will be disassembled and shipped to the site of the Coringa project. Payment is structured in several payments, however $2.0 million will be paid out in June 2016 to finish the deal. It will be processing ore with an average grade around 8 gm/ton, considered high grade gold.

The Team

The management team consists almost entirely of the crew from Lumina copper. The same team that got Ross that 100 bagger. They have done it before and are now positioned for the next challenge. Whereas the Magellan team were competent developers who simply ran out of financing at the bottom of a bear market, Ross and his team step up to advance the project with financing and the stature that comes with one of the most respected tycoons in the industry.

The Strategy

The Anfield team has been very tight lipped about their plan. No one from Anfield showed up at the meeting and I made it a point to ask each of Magellan’s officers what they were up to. Amazingly, none of them knew any first hand information only their own opinions and frankly they didn’t know of Ross’s grand strategy. They had no knowledge of Ross’s position in Condor gold in Nicaragua. I guess that’s why we call them operators and consider ourselves market strategists. My observation was they were happy to get rescued and hadn’t though much about the deeper implications of what is up here.

Interesting to note that I was told by the individual who would know that Eric Sprott had kicked the tires on this project also and almost bought it, but was too tied up with his Newmarket gold and Kirkland investment. So that’s more anecdotal information confirming the value here. I also find it very revealing that Anfield retains Nickel in its name. Recall they have no Nickel, but the title stays there. Knowing how easy it would be to change the name one must think it serves a purpose to keep them off peoples screens for now. The word is they are going to change it to Anfield Gold, at some point in the future. (edit …this is fait accompli .)

First production is planned in the second half of 2017. This was described as very aggressive by the Magellan guys, but doable.

—end post (edited for brevity)

For those holding out on coming on over and joining the Spock site I ask “do the math”. I personally had bought 90,000 shares of ANF. In just this past week alone that resulted in a $40,000 payoff in that position. Not bad for an afternoons trip to Vancouver, but even better it was nice to get the scent of Mr. Market and beat him at his own game.

Rick Rule owns stock in his personal account it appears. So although Sprott Corporate did not do the deal, Rick made sure he bought some stock. Sprott may also get involved in the financing down the track. Rick is saying they may rename again to Lumina Gold.

This is a district new gold camp play, and I can see some further acquisitions in the pipeline already. I am doing checks on the possible targets now, as they could be bought for a premium … some cream on the cake.

Its all about having information, then joining the dots, being one step ahead of Mr. Market.