A VERY VERY important piece of news hit in the energy space that nobody noticed

http://www.ft.com/fastft/2016/04/19/crucial-coal-benchmark-deal-tops-expectations/

The spot prices for coal are too low and not the REAL price. This is Australian Thermal, but you get the picture.

“One of the most important deals in the commodities industry has been signed with Japanese utilities agreeing to pay a significant premium over the market price to secure supplies of high-grade Australian coal.

Tohoku Electric Power and Glencore, one of the world’s biggest producers and traders of thermal coal, have settled their annual price negotiations at a price of $61.60 a tonne – more than $10 above the spot price and ahead of analyst expectations, writes Neil Hume, the FT’s Commodities Editor.

“This marks the largest premium to spot that we have on record (i.e. in at least 15 years),” said analysts at Macquarie.”

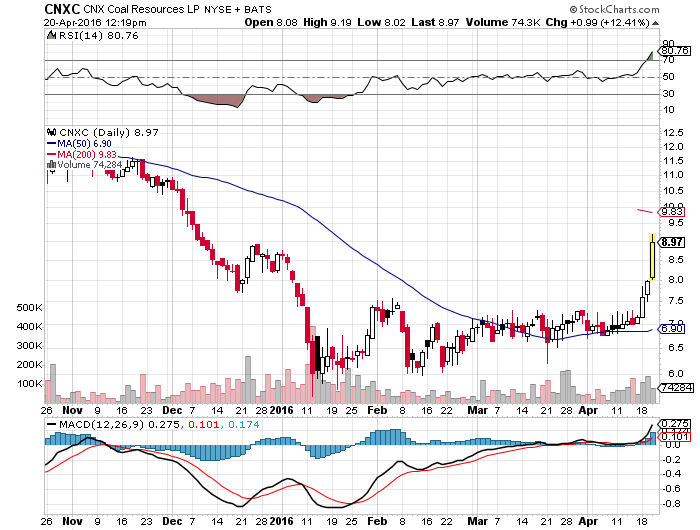

I have been pounding the table on CNXC for a couple of months. It’s starting to go. Every way that I model it from a fundamental standpoint, this LP is worth 20+. With the bankruptcy of Peabody, coal has bottomed.

Thanks Cashcosts…strong fundamental thesis…

Thanks very much for sharing your excellent fundy analysis. Bought some a while back, and doubled position on the open today. Had guessed there was some anticipation of quarterly result (and divvy announcement??) on Monday, but your article implies broader trend. Parent (Consol) ripping away today as well. Cheers

What set these things going was SXCP’s announcement that they were retaining their full distribution. If CNXC comes out in the next week and maintains their 2.05 yearly distribution on a quarterly basis, then I expect to see another leg up. We could be back to the IPO price of 15 in a hurry. There is so little float… Einhorn owns half of the units.

nice one Cashcosts. Keep up the great work.

Excellent work, thanks for sharing-