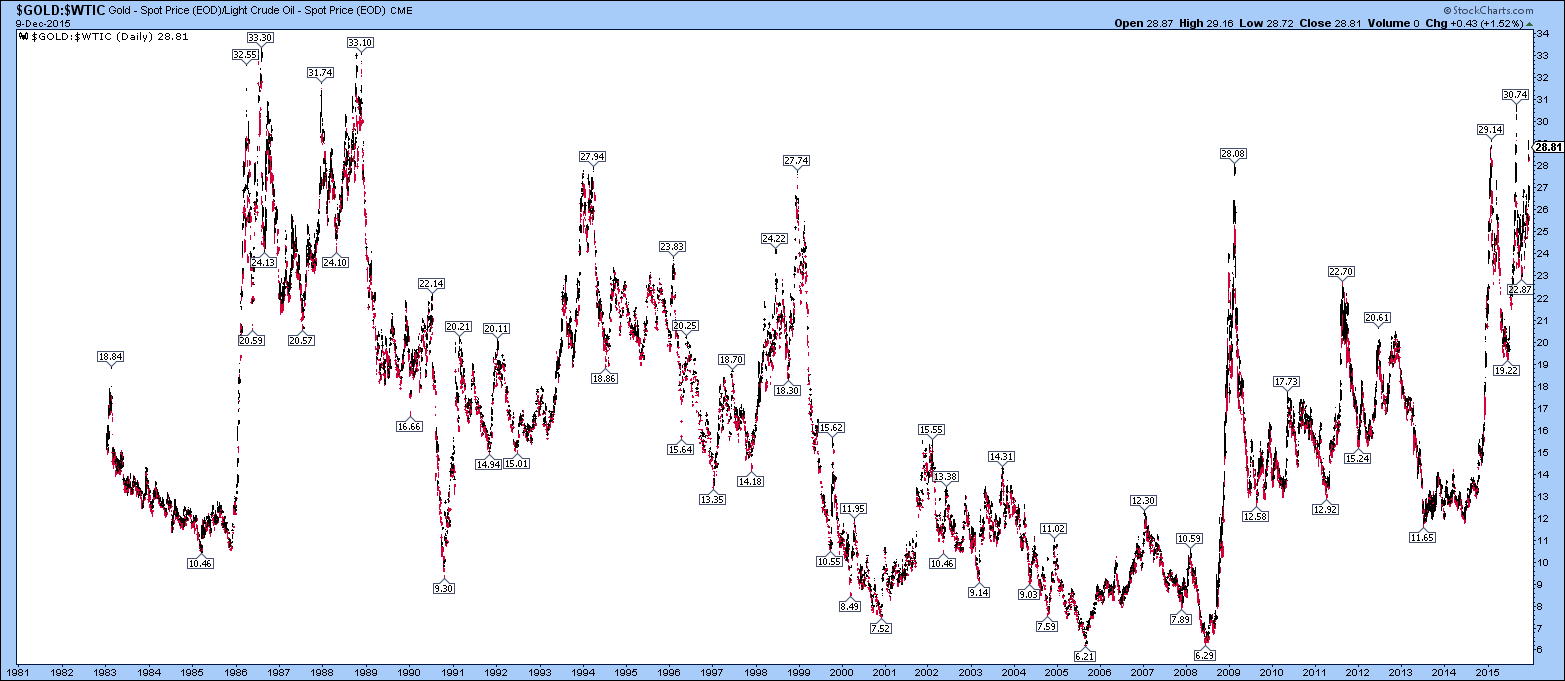

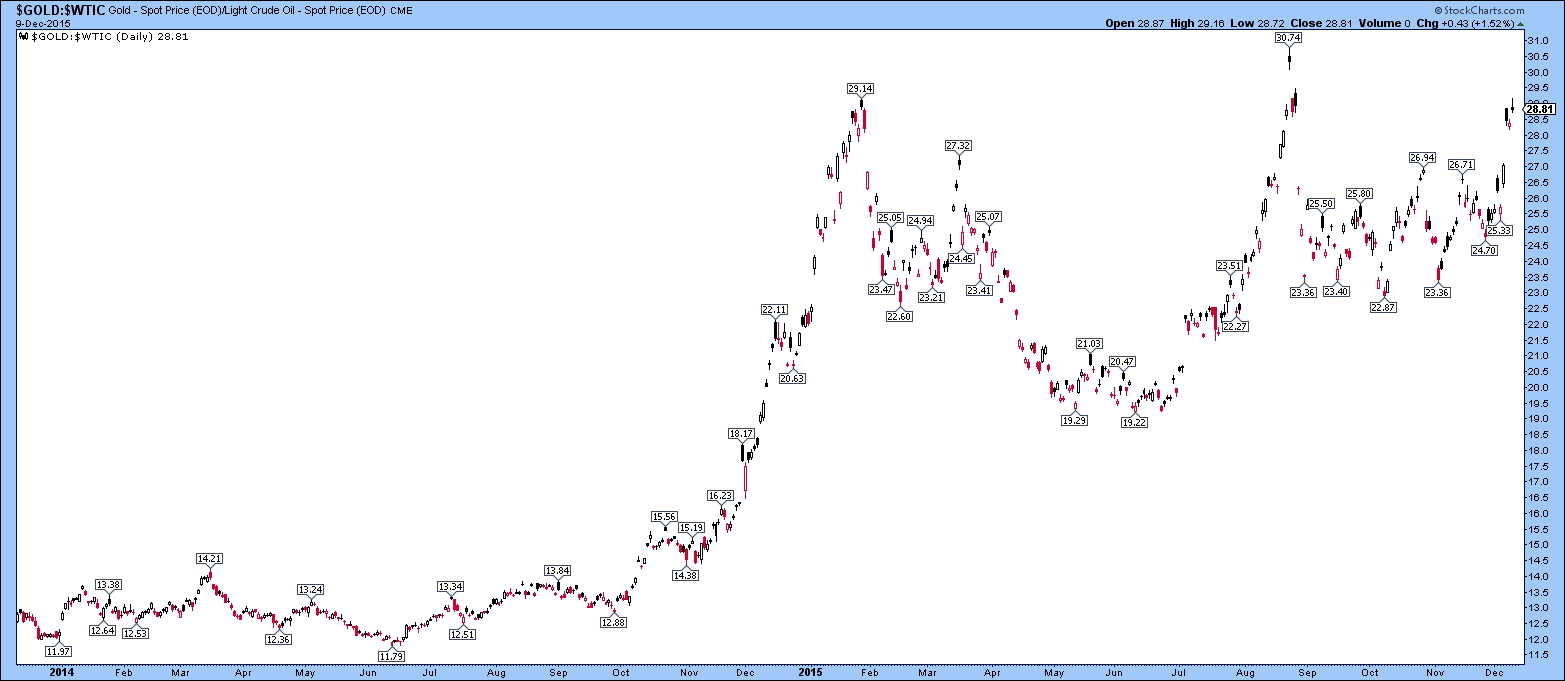

What’s happening with gold:oil ratio?

I find it difficult to be bullish on gold right now (as perhaps most of us do) but the main point is that the dominant theme at the moment is the expected further falls in WTIC oil.

Looking at the gold:oil ratio, for gold to stay above $1000 with oil at $30, gold:oil needs to go to 33.3. Now that would be within previous action over the past 35 years or so. over that period, that highest value of 33.30 was in 1986.

However that would be “resistance” so to get away from that figure again to the downside either a good rally in oil or a good fall in gold would be needed to “normalize” the ratio.

The alternative would be to have gold:oil break out above the 30-33 ratio that has been resistance for the past 30 years. This would almost coincident (by the way!) to the US dollar index USDX breaking above its 30 year resistance line from 1985.

To me this is an interesting fundamental event. If we have a deflationary credit crisis as I believe we do, we can perhaps expect events to happen that have not occurred since the 1930s when the last deflationary crisis occurred. I haven’t got any data on the gold:oil ratio in the 1930s but I guess that it went up sharply as gold was revalued from $20.67 to $35 in the 1933-1934 timeframe.

interesting analysis. oil is a big cost of mining, as it is used for power generation, mining equipment operation, explosives, tires, you name it. so a rising gold:oil ratio, or gold:CRB ratio is good for the gold miners.

HI Spock, Thanks for the reply. Bob Hoye has been onto that one for a long time with his ‘real price of gold’ – is gold divided by a commodities index, something similar to the Economist All Items Index as a proxy for the real price of gold instead of gold related to the CPI for instance. Unfortunately as far as I can see, that hasn’t worked, since gold:CRB is higher than in 2011 but gold stocks have been slaughtered. Same for gold:oil ratio which was 22.70 in late 2011 and is now higher at 30.6 yet gold stocks have been slaughtered since then: HUI has gone from 600 to 116.

So to me only the gold price in US dollars really matters, except that gold ;price in the local currency where the costs are located is also really important (e.g. on the big fall in the South African Rand sometimes in late 2001 or thereabouts, their local gold price rocketed and so did their gold mining stocks).

I think the gold:oil or gold:commodities ratio works in a gold bull market when it adds juice to the gold stocks. However in a gold bear market (versus US dollars) generally these ratios don’t define the trend – the USD gold price does. I mean oil could go to 0 but if gold went to $500, just about every gold company is probably out of business even though the gold:oil ratio is infinity.

I guess that is because many of the costs of gold miners are related to other things like wages, regulatory costs, certain infrastructure costs like equipment, taxes, security, blah blah blah. If oil is 25% of the cost of mining and commodities are another 25%, the other 50% is something else that is either priced in local currency or US dollars and is likely to rise as inflation is still above 0 in most countries. So in falling USD gold price scenario, gold stocks generally do no good, period.

Unless you are a great trader and watch the best companies closely that will do OK in any market because they add value.

Just my twopennyworth! I have just started to read your posts by the way. Really interesting, as is much of the material on this site.