TOM LUONGO

Love him or hate him …Luongo has become a must. I strongly recommend a subscription to his Patreon Blog

He puts out a Barnburner Monthly Essay every month that is for subscribers only .

Something to be aware of Luongo used to treat Trump as a Buffoon and was not on board with him for the most part …until 47 BURST on the scene

In his videos the guy is prolific and Brilliant and Passionate ..Profound and Profane ( very Profane )

But his monthly piece is All Business

…….

Here is his opener…the rest I will post in the comments ( stand by …the formatting is challenging )…but get a subscription…

…………..

The rules of the global game of capital flows are changing daily.

President Trump is making a series of bold moves to rebalance

the field not just for the ordinary American, but ordinary people

the world over.

A global financial system does not have to look like the one

we’ve lived under, with people pushed around like meeples on a

brightly-colored board serving the whims of unseen oligarchs.

Sports used to reflect this before it got lost in the same cheap

money shuffle like everything else. It should be a celebration of excellence, of local

pride and passion, not mercenaries bouncing from place to place with nowhere to call

home.

Trump really believes in that schmaltzy stuff, and it is what ultimately drives him,

even if he may not understand what he’s unleashed. This month’s issue looks at

Trump’s tariffs in the context of the bigger game and what the next moves by all the

players looks like

……………………….

In today’s egalitarian world, any moment of pure

excellence should be celebrated more than ever. As a hockey

guy I remember when Alexander Ovechkin was drafted by the

Washington Capitals.

Leading up to draft day the #1 overall pick is almost always put

on a scale of becoming “The Next Gretzky.” Few come close to

living up to that moniker. Every once in a while a generational

talent comes along that even the most cynical hockey fan can’t

ignore. We were blessed with a bevy of them twenty years ago.

“Ovie,” a Russian, was drafted in 2004. Sidney Crosby, a

Canadian, was drafted the next year by Pittsburgh, after the

lockout. They were the subject of endless “who’s better?”

discussions with Ovie getting thrashed by traditionalists

because Russians don’t really love the game. It was Hockey’s

new Cold War.

He was the least liked great player in the game’s history,

because he didn’t come from hockey royalty.

Ovechkin changed our perception of what a hockey player

could be; the total package of size, speed, strength, and

tenacity who continues to play the game as a graybeard with an

enthusiasm that is rare in the world today.

Ovie gave way to “The Great 8” when he led the Caps to their

only Cup in 2018 and he’s trying again this year leading the #1

seeded Caps into the playoffs.

We will look back in awe at what he did. An Alex O highlight

reel is a thing of beauty.

In the twilight of Alex’s career, it is important to think back to

another Alexander, Mogilny, the first Russian to defect to the

NHL from the Soviet Union in March 1989. It was a different

world then, but Mogilny’s courage paved the way for Slava

Fetisov’s defection two months later which were harbingers of

the soon-to-be post-Soviet world.

And because of them, NHL hockey has never been the same.

Good. While the old guard complained bitterly on Hockey

Night in Canada for years to come, ultimately, the game didn’t

belong to them. It belonged to the people who played it and

the fans who supported it. Just like Davos isn’t the economy,

and we’re just cogs.

Systems either evolve or die. And the global financial

oligarchy’s sad attempts to resurrect the Cold War to maintain

their system shows just how close they are to dying. The

Soviets ran into this with Mogilny, Fetisov, Konstantinov and

Larionov. And now Davos is running into it with Donald Trump

and a US electorate tired of being taken for granted.

We would hope they have enough respect for the game as Alex

did by not scoring the record-breaker into an empty net and

Gretzky did by being the first person to congratulate him doing

so.

The Tariffs Heard ‘Round the World

On April 2nd, which Donald Trump christened “Liberation Day,”

he unveiled the new reciprocal tariff structure to do business

with the US on a county by country basis. Trump’s new

schedule ranged from a minimum of 10% to a high of 49%

charged to Cambodia.

What Trump and his team did was include in their calculations

the current trade deficit with the US and add half of that to the

tariff baseline of 10%. The math wasn’t hard for anyone to

figure out. Methinks that was the point.

For months Trump has been warning the world that he would

do this yet somehow everyone was surprised by what he

presented. His messaging up until April 2nd was simple, make

a deal with the US or we’ll tariff you to claw back part of that

trade surplus.

And the result of this was more than a week of temper tantrums

from all corners of the financial markets. The administration’s

messaging was consistent. They were unperturbed by equity

market turmoil or even the possibility of a recession. This was

a necessary first step in changing the direction of trade flows.

The market reaction was one of disbelief. A lot of people were

on the wrong side of a lot of trades. At the same time the

performance of US equity markets in Q1 reflected smart players

taking Trump at his word and selling early. All the major US

indices underperformed the rest of the world.

So, equities already had the jitters. It doesn’t take much to

push jittery markets over a cliff. Trump decided to use a

bulldozer.

While Trump was erecting trade barriers, uncovering wasteful

and fraudulent government spending, and pushing for tax and

spending cuts, his counterparts in Europe, China and Canada

were pledging to spend, spend, spend. Under that macro

environment future dollar flows should be lower and future

euro flows larger. That’s what the policies are saying.

So, it should be no surprise that there was both a run on

European sovereign debt and into European equities and a

simultaneous run out of US equities and into US bonds overall

by the end of Q1. If that was all that happened and everyone

went back to their benches to do their own thing, accepting the

new reality, then this wouldn’t even be worth discussing.

But that is not what happened. The confrontational rhetoric

coming collectively from the EU, Canada, and China along with

their announcements of escalating tariffs defined the state of

play.

“Liberation Day,” was the financial shot across their bow.

Within hours everyone Trump had singled out previously tried

to quickly offer, “zero for zero” tariff deals which Trump

rejected immediately. Smartly, he moved the goalposts and the

messaging to highlight everything that goes into erecting trade

barriers, the real cause of these trade imbalances.

But he got a lot of phone calls, enough so that he put a 90-day

hold on anyone who rung him up. They still got the 10% tariff,

however. That is the new price to do business with the US.

Trump is many things, but stupid is not one of them. He knew

what his target was and hit bullseyes.

By the end of the first week after “Liberation Day” we had

clarity as to who was and who wasn’t willing to work with the

US. For someone like Trump who must build political capital

today to pull off the rest of his plans in the 2nd half of this

term, that clarity was necessary.

Viewed from that lens it was worth a few days of turmoil which

stripped a couple of thousand points off the Dow and added a

few basis points to the yield on a 10-year US Treasury Note.

The Basis of the Davos Trade

Davos et.al. responded with a brutal attack on not only the US

equity but, more importantly, US bond markets. We were told

initially it was China selling. Then there were rumblings of the

so-called “basis trade” which is essentially pocketing the few

basis point (each basis point is 0.01% in yield) spread between

US treasury futures contracts and the spot price.

That basis trade was only part of the story and the full cross

market analysis of trading starting on April 9th through to the

close of markets on Friday, April 11th is more complicated than

that.

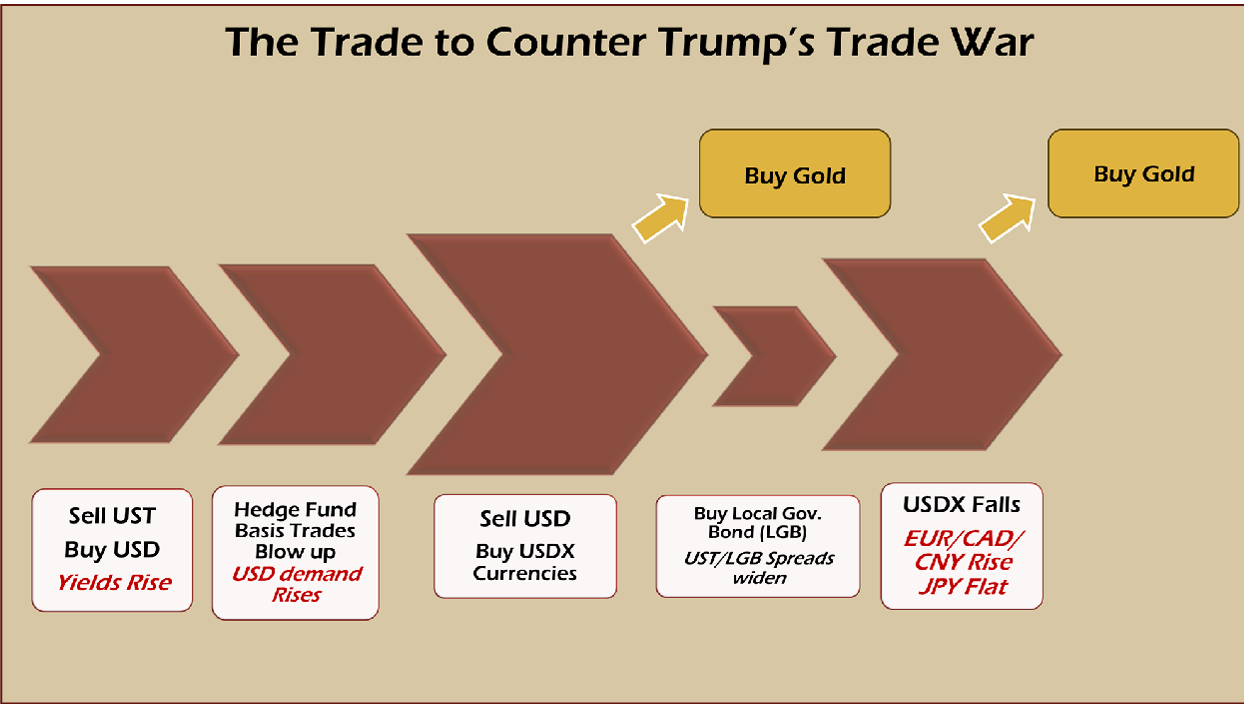

Any selling that occurred would trace itself back to the seller

through shifts in the foreign exchange markets. It would show

up in the currencies. Anyone selling would see their currencies

rise sharply and anyone who didn’t wouldn’t.

As I pointed out in the Market Reports from April 9th and 13th,

the smoking gun was we saw big moves in the US Dollar Index

(USDX) which is primarily made up of the euro (EUR), British

pound (GBP), Canadian dollar (CAD), and Japanese yen (JPY)

and not in the Chinese Yuan (CNY). The conclusion then had

to be that the selling came from them and not primarily from

China (see graphic).

During this turmoil some of the excess cash would signal to

some to park that cash in gold, especially with the US dollar

falling as quickly as it was.

Once the basis trade entered the conversation there was

another head fake concerning Japan as that dominated for

about a day. The story, and I’m sure there was some truth to it,

was there was some selling coming from there. But whatever

selling occurred it wasn’t enough to move the yen as much as

we saw in the EU centric space.

I’m not ruling out China selling US dollars to help this trade

along but as I’ve pointed out many times, it has been the EU,

Great Britain and their proxies that have been gorging on US

debt since the Fed began raising rates in 2022.

China’s ~$750 billion US Treasury reserves pales in comparison

to the ~$3.8 trillion held by our “European partners,” to quote

Russian President Vladimir Putin.

What is important here is that, in my opinion, Davos isn’t

finished attempting to maintain its leverage over our financial

system in this new era of finance. That new era is defined as

Europe and City of London no longer having the direct ability

to manipulate the price of US dollars flowing through their

markets

SEE GRAPHIC IN THE MAIN POST

Raids on US bond markets are the primary mechanism by

which to force the Federal Reserve to act. As I’ve said many

times, the Fed will not react to problems in the equity markets,

certainly not under Jerome Powell. It will, however, act if there

is an attack on the US bond market.

Blowing up a dormant basis trade or two, lurking like

unexploded land mines in a field, has worked in the past to

force the Fed into action. The SOFR crisis of September 2019

forced the Fed to open up its Standing Repo Facility to

commercial banks to provide temporary liquidity.

Then in March 2020, when the markets seized up over

COVID-19 and the collapse in oil prices, the Fed was forced into

a far greater move; back to the zero-bound and monetizing a

great deal of the debt issued supporting the CARES Act. They

had to do this because the market for US treasuries completely

seized up and the Fed was the only buyer.

Both of these events occurred during a period where SOFR

wasn’t dominating markets, when interbank lending was

uncollateralized. Today that is no longer the case. All vestiges

of the old LIBOR system are gone. And now SOFR’s ability to

stabilize domestic US dollar markets has been tested.

I have to speculate that Trump and Treasury Secretary Scott

Bessent understood this as the

timing of “Liberation Day” just

two days after the last synthetic

LIBOR contract expired seems

suspicious.

I won’t pretend to know what

really happened but a quick

perusal of the 3-month SOFR

Futures intraday trading

revealed massive selling

pressure in the March, September, and December 2025

contracts when markets opened on the evening of Sunday, April

6th. During normal trading SOFR moves 2-3 bps per day.

During this week, at key times we saw 1-hour trading ranges of

20-30 bps.

For that entire week there was relentless pressure on the long

end of the US yield curve, and Trump responded by backing off

on his huge tariff increases on everyone except China and the

EU.

ZO-PAAAA!

Did Trump overplay his hand, or did he flush out who his real

enemies are? Because moves like this leave a paper trail.

Money flows of this size have a memory. Knowing Trump’s “Art

of the Deal” style, it would seem a bit of both. He starts well

above his intended goal, outside of the Zone of Potential

Agreement (ZOPA), gets his opponent to make a big move, in

this case creating a massive panic in our financial markets, and

then backs off a little bit after they reveal how far they are

willing to go to win.

In other words, this was a recon mission. Let’s find out just

how vulnerable everyone is. You can’t fight a war without

intelligence. You also can’t fight a war if you don’t know where

your vulnerabilities are as well as your opponents’.

At the same time, however, the best way to win a fight, as I was

taught in martial arts class a lifetime ago, was to go first. If you

know a fight is inevitable the best thing you can do is put your

opponent on the defensive. So, to me, this strategy makes the

most sense for Trump; keep his opponents guessing as to what

he’s going to do next, make them react, and prep the ground

for the next battle.

And if they come back at you with a barrage that bloodies you a

bit, respect it, retrench, and get ready for another round.

On the opposite side of the ledger Davos is known for not

backing down on anything. Their modus operandi is to be

aggressive but blame their target for defending themselves.

They issue ultimatums. Their negotiating style is always to ask

for everything but give nothing. We saw this with Greece’s debt

crisis in 2015 and with Russia’s concerns in the run up to Feb

2022’s initiation of conflict with Ukraine. If Davos are told no,

their response is always to destabilize the target country

through soft power and financial attack and then blame their

victim.

Their arrogance and their perception of a dominating position

is both a strength and a weakness.

The moves we’ve seen China make are rooted in the Asian need

to save face in all confrontations. Trump knows he has to press

China into a corner to get Xi Jinping to the bargaining table.

China understands that Trump’s overtures to mending fences

with Russia is a de-escalating move towards China as proxy.

Russia is a key partner for China across many areas – energy,

commodities, food and defense.

Xi understands, like Putin, that

the old power centers of Europe

are their implacable enemies.

The EU’s rearming to take on

Russia in the future is an attack

on China, ultimately.

Because if Putin falls in Russia

and the country carved up into

pieces, long the plan of Davos and City of London, then the

wealth of Russia no longer flows East but West.

This gives Trump a lot of negotiating cache with China when

the time comes.

So, along this vector, Trump and Xi are aligned. It’s why I don’t

see a major conflict between the US and China, because it

would only strengthen the dead hand of Davos and Europe.

That said, China is also not going to bet the farm that Trump is

wholly successful in liberating the US from Europe. So, they

will keep the pressure on Trump in trade talks, knowing full

well that in a tariff war with the US they can dump their

cheapest crap on the EU just as easily as they can on the US.

China will play the waiting game for as long as they can.

The Playas Who Also Hate the Game

Everyone in this game knows that whoever loses here, loses in

the long run. China is struggling to convert its export-driven

economy to an internal consumption model, the US is staring at

an investment deficit that would break our political union when

the debts can no longer be serviced, and the EU is staring at a

collateral deficit in the form of energy and raw materials which

can only be overcome with a new round of colonization of

primary producers.

All of these major power centers are staring at real

demographic crises where there aren’t enough new workers to

replace those their economy must currently support. Meaning

they are all fighting a structural deflation that can only be

reversed by liberating the creative impulse of their people and

making them secure enough in their futures to have babies.

Trump’s domestic plans are aimed at doing just that.

As for the other players at the table, they have already chosen

their sides.

Japan will keep Trump as happy as possible because they are

the poster child for demographic deflationary collapse. Prime

Minister Shigeru Ishiba has already pledged to work with

Trump on Japanese investment in America. Honda (HMC)

recently announced they are moving a key production line from

Ontario to the US. Back in January Softbank pledged a $500

billion investment in the US. Japanese automakers are already

some of the most MAGA companies in the world, making cars

in all of the low-tax, low-regulation states in the US.

Canada’s role in this is simply as a pawn to be sacrificed in the

process. Sadly, nothing more. If Mark Carney wins the election

expect another, bigger attack on our bond markets as we move

closer to the debt rollover cliff, some $8.9 trillion, this summer.

Davos’ main goal is to force the US into another moment like

this one as soon as possible. Trump and Bessent want to

refinance that debt at low rates over a long time, which will

give them the breathing room to fix the budget deficit quickly.

If Bessent is forced to refinance that debt with more short-term

issuance, less than 5 years, it creates another crisis date for the

US going into the 2028 election cycle. It also harms their

political position going into the 2026 mid-terms.

The big wildcard is still Italy as Prime Minister Giorgia Meloni

has successfully walked a tightrope during the Biden years to

survive into 2025. She came to D.C. this month to discuss a

bilateral trade deal with the US over the strenuous objections

from the EU.

Her visit may become a watershed event, like Alexander

Mogilny’s defection to the NHL, which marks the beginning of

the end of Europe’s political solidarity.

Moves like these, which imply the old order of power and

leverage is weakening, could ultimately tip the balance of

power in the world. By the end of this month Trump will have

moved away from tariffs and trade deals to peace negotiations

with Russia and Iran.

That old order was based on the illusion of free markets and

misdirection. With his tariff gambit Trump changed the entire

nature of the game of global capital flows. He laid bare

everyone’s weaknesses, including the US’s.

What comes next will be another round of escalation. Davos

has a summer of misery planned for the US, similar to 2020’s.

The game has changed. The outcome is in doubt. But at least

we’re getting the chance to play

Tom Luongo

this seems to be the bottom line:

Everyone in this game knows that whoever loses here, loses in the long run.

China is struggling to convert its export-driven economy to an internal consumption model, the US is staring at an investment deficit that would break our political union when the debts can no longer be serviced, and the EU is staring at a collateral deficit in the form of energy and raw materials that can only be overcome with a new round of colonization of primary producers.

interesting further takes

Yakubu Agbese

@YakubuAgbese

You’re right that it is game theory.

The problem tho, is that you think the opponent is China.

Trump’s counterparty is the financial markets.

How do we know?

Because the confusion created is coursing through financial markets, not Zhongnanhai.

He’s bluffing us. Not them.

In Bayesian games, bluffing can be effective

The problem tho, is that getting caught in a lie signals fear I

In this case, lying to Wall Street tells the market that it has leverage over the President

Which means China can just sit back and let Wall Street negotiate in its stead