Late reporter for Q4…APM.TO

Look at this growth, year over year…41 million to 115 million

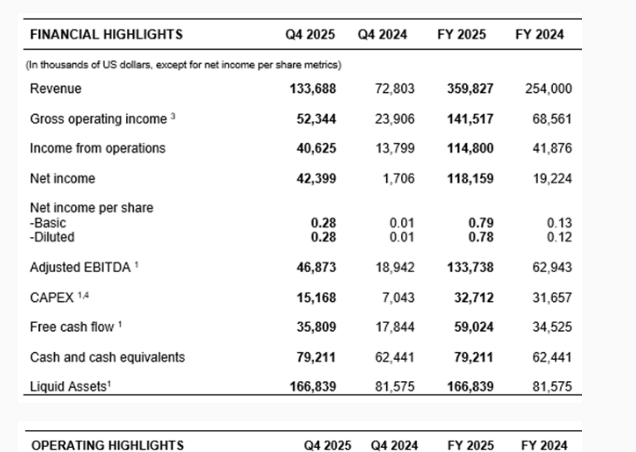

Keys from release, IMHO. Once again, they are selling direct to somebody who pays more than the crimex prices.

Record realized prices: In the fourth quarter the Company achieved an average realized gold price of $4,171/oz and average realized silver price of $59.88/oz, both higher than the spot market averages for gold and silver prices of $4,167/oz and $55.29/oz, respectively.

We also expect several important milestones in the year ahead, including the planned listing on the New York Stock Exchange and the release of an updated technical report at Golden Queen, which we believe will further enhance the Company’s visibility and profile with the global investment community.”

Negative – Guidance for next year is not a huge growth in GEO’s, but the prices will be higher if gold and silver continue their upward trends.

The Company expects consolidated production to be between 100K and 114K gold equivalent ounces in 2026, based on an 85:1 gold?silver ratio, comprising between 46K – 54K ounces of gold and 4.6 – 5.1 million ounces of silver.

Chart – on sale like many quality juniors. Filled the gap from September just 2 days ago, wowzers.

I thought this was interesting from Grok. The entire analysis was quite long so I just put in this final summary. I have these three and was wondering how they compared to each other:

Overall Ranking for Most Potential (asymmetric upside from here)Minera Alamos (MAI) — Best risk/reward balance: current production derisks it, pipeline is permitted/low-capex/self-funded, valuation cheapest relative to peers, jurisdictions strong. Watch for Gold Rock/Copperstone PFS updates and reserve expansions.

West Red Lake Gold (WRLG) — Very close second for pure-play believers. Newly producing with high-grade leverage, Rowan/Fork catalysts, and combined PFS ahead. Strong operational momentum post-restart, but monitor 2026 guidance and ramp to full capacity. Excellent “hidden value” story in a bull market.

seekingalpha.com

Andean Precious Metals (APM) — Respectable for diversification/FCF, but least torque — higher costs, mixed jurisdictions, growth less transformative.

Recommendation: I’d still allocate heaviest to MAI today for the cleanest multi-year compounding story. Add WRLG as a complementary high-grade Ontario bet, especially on any pullback or post-guidance clarity — it could re-rate hard if ramp hits targets and gold stays elevated. APM is fine for balance but offers the least relative upside among the three.

I have all three, so….but yes. DD likes MAI.V and has for some time. If you look at the charts, Andean and WRLG are selling at Sept 25 levels and MAI.V is back to Jan 2026 levels. All good, just have to make a choice if you can own only one.

I added 1911 Gold to the mix and Grok said it should be considered 2nd best on the list over West Red Lake Gold. Grok showed a lot of excitement over it as well. It seems to be floundering though as of late. I’m sure it will catch up soon.